Please, see the black arrow below

Yellow vest

Liberty, Unity, Friendship

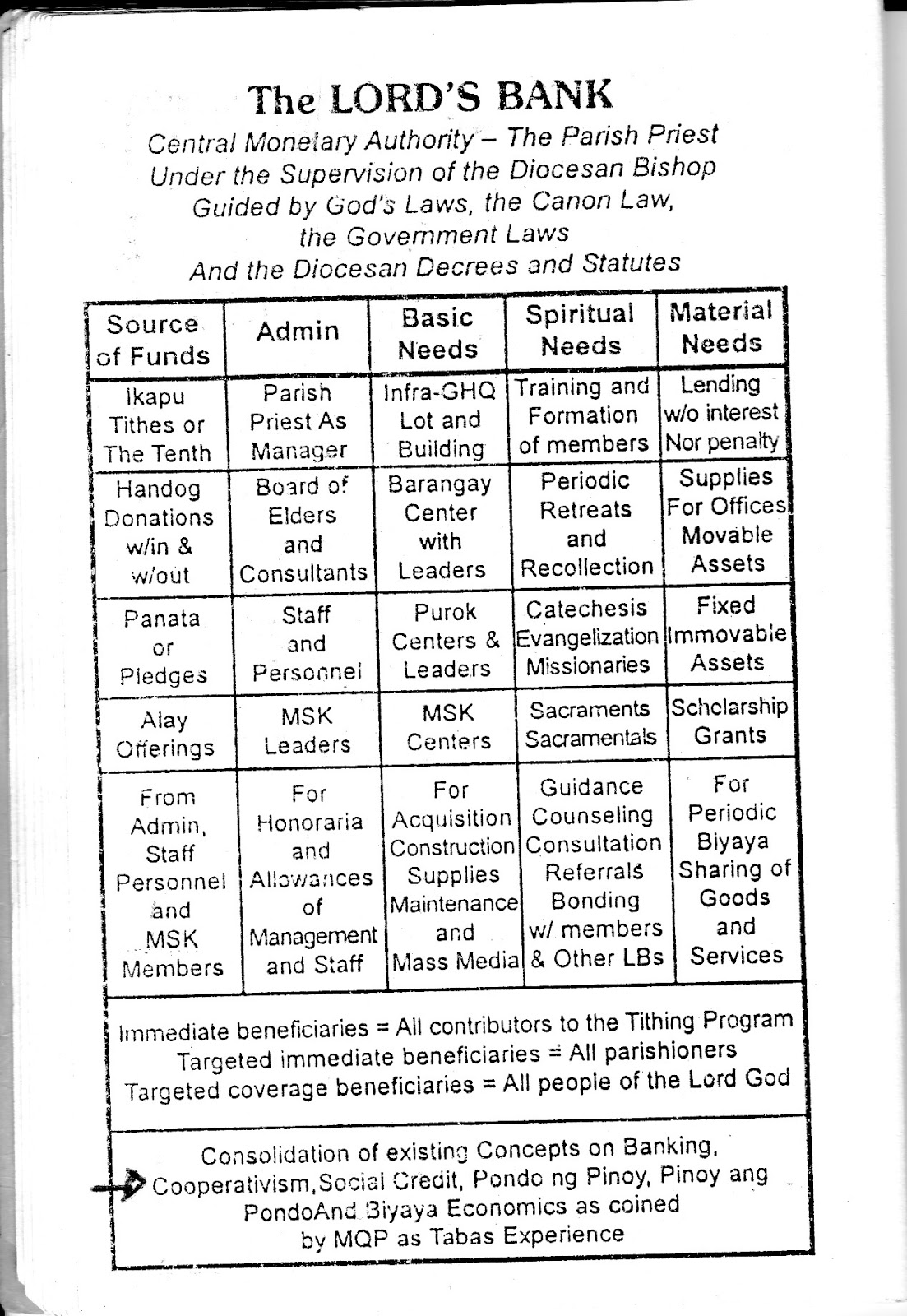

Philippines. The Lord's bank

Economical democracy in the Philippines.

inspired by social credit and swiss www.wir.ch

See the arrow

... he read about WIR, the Swiss complementary currency, and became ... There is no bank that prints Sardex notes; no algorithm that ...

Sardex, an emerging model for credit clearing exchanges?

https://www.sardex.net/?lang=en

Last week I had occasion to visit the Italian island of Sardinia and spend a few hours meeting with the founders and managers of a commercial trade exchange called Sardex. Here below is an abbreviated report of what I learned. The pdf version of the report can be found here.

Sardex, a brief report

by Thomas H. Greco, Jr. August 15, 2015

I recently spent a few days on the Italian island of Sardinia conferring with the founders and administrators of Sardex ( https://www.sardex.net/?lang=en or http://www.sardex.net/), a commercial credit clearing exchange that has been notable for its success in organizing small businesses and service providers on this island of about 1.6 million people.

I’ve known about Sardex since almost its beginning five years ago and have corresponded over the past few years with Giuseppe Littera, one of its founders, but this was the first opportunity I’ve had to get an inside look at their operation. I came away with a pretty good understanding of how they operate and the impression that the Sardex structures, procedures, and protocols come closer to optimal than any other trade exchange I’ve seen. It appears to be a developing model that is both scalable and replicable.

I will not attempt to provide here a comprehensive report or detailed analysis, rather I will highlight a few major points and provide some sources of additional information for those who are interested in doing their own research.

Some highlights:

Current membership: ~3,000

Current transaction turnover: ~1.5 million euro equivalent per month

Expected turnover for 2015: 50 million

Velocity of credit circulation: 12 times per year

Employees included as sub-accounts: 1,000

When I asked about the key factors that account for their success, here is some of what I was told:

1. Founders are dedicated to the mission to relocalize and rehumanize the economy and to reconnect people by enabling the creation of interest-free local liquidity based on the production capacity of local businesses.

2. Social solidarity and cultural cohesion, while very important and part of the mission, were NOT a pre-existing factor that would account for their early success. In fact, they have had to work hard to develop social solidarity and cooperation amongst their members, but this is now changing. One account broker told me, “I can see how behavior of many of our members has changed. When the financial crisis first began, they were starting to lay off employees or cut their wages, and they were reluctant to spend their euros. This made matters worse as the circulation of money slowed down. But as they began to participate in the process of earning and spending trade credits, they began to increase pay to their workers and to invest in their education. In one case, when a member’s shop was burglarized, other members stepped up to help by donating some of their trade credits to help their fellow member recover from the loss.”

That anecdote demonstrates the differences in behavior that results when people experience scarcity compared to when they experience abundance. In this case, the scarcity of euros caused behavior to change in the direction of reduced willingness to spend and the contraction of overall economic activity. But their experience with trade credit was much different. Realizing the greater availability of trade credits, and finding it easier to earn them, leads people to experience abundance and to be more generous and spend more liberally.

3. I was surprised to learn that the Sardex revenue model relies mainly upon initiation fees and annual membership fees (collected in euros); and that they had decided early-on to stop charging fees on transactions. For me, that approach is counter intuitive in that I have long held the view that recruitment would be most successful if membership were made easy, low cost, and risk free, and that it seems reasonable to apply the principle that users pay in proportion to the amount of services they receive. In this case, that principal would mean that those that receive more credit clearing services should pay more. Well, this may be a case where successful practice trumps rational theory. Marketing specialists should look closely at the dimensions of this phenomenon.

There is however some logic in this approach in that, since the cost of participation is relatively fixed, members should seek to maximize the benefits of their membership by trading more within the network. Initiation fees are set according to the size of the business and range from 150 to 1,000 euros. Annual membership fees are likewise based mainly on turnover and range from 350 to 2,500 euros.

4. Strong member support by an effective staff of brokers who help to arrange trades, especially for those that have high earning capacity to avoid excessive accumulation and high positive trade credit balances.

5. Recruitment strategy tries to replicate the supply chain, i.e., bring in businesses that are the suppliers of existing members or prospective members.

6. “Solidarity threshold.” Requirement that members offer their goods and services for trade credit at the same prices as their euro prices, and that payment be accepted 100% in trade credit on all transactions of less than 1,000 euros. “Blended trades,” i.e., payment in a combination of trade credits and euros are allowed on larger purchases, according to a sliding scale).

7. (a) Restrict membership to companies that have a registered office in Sardinia. This promotes social solidarity and excludes large multi-national corporations. (b) Avoid “saturation” (accepting too many members that offer the same line of products or services).

[While I am fully supportive of the former of these, and would indeed, permanently exclude multi-national companies, this latter practice of avoiding saturation I consider to be of use only in the initial stage of establishing credit clearing as a credible means of exchange and an effective source of local liquidity. Ultimately, I believe that membership must be open to any community-based small or medium enterprise (SME) that meets the basic qualifications for membership. Of course, not all of them will qualify for lines of credit.]

8. Fully compliant with reporting and tax regulations. Transparency is a matter of fundamental importance.

9. Emphasis on monetizing the unused capacity of members. Connecting unused supplies with unmet needs is a primary benefit of credit clearing services.

The Sardex company has been consulting with other groups to replicate their system in seven other regions around Italy. In the future, Sardex is planning to initiate a rebate program to bring consumers into the trading community, which will enhance the circulation of local trade credits, make Sardex better known, and stimulate more sales for their business members.

Here below is a list of a few of the many reports and sources of information about Sardex. Readers are invited to add others as comments

From an idea to a scalable working model: merging economic benefits with social values in Sardex, by Giuseppe Littera, et al, at the London School of Economic, Inaugural WINIR Conference, 11-14 September 2014, Greenwich, London, UK.

You can get a pretty good picture of the distinctive features of Sardex by viewing Giuseppe Littera’s presentation that was made (in English) at a conference in Volos, Greece, in 2014. It is to be found on YouTube at, https://youtu.be/rvaL2A8juz0

Report (in Italian) in the Italian daily newspaper, La Repubblica: Dalla Sardegna al resto d’Italia. Sardex inventa la moneta complementare. “Abbiamo ripensato l’economia.” [English translation needed.]

https://www.sardex.net/?lang=en

Last week I had occasion to visit the Italian island of Sardinia and spend a few hours meeting with the founders and managers of a commercial trade exchange called Sardex. Here below is an abbreviated report of what I learned. The pdf version of the report can be found here.

Sardex, a brief report

by Thomas H. Greco, Jr. August 15, 2015

I recently spent a few days on the Italian island of Sardinia conferring with the founders and administrators of Sardex ( https://www.sardex.net/?lang=en or http://www.sardex.net/), a commercial credit clearing exchange that has been notable for its success in organizing small businesses and service providers on this island of about 1.6 million people.

I’ve known about Sardex since almost its beginning five years ago and have corresponded over the past few years with Giuseppe Littera, one of its founders, but this was the first opportunity I’ve had to get an inside look at their operation. I came away with a pretty good understanding of how they operate and the impression that the Sardex structures, procedures, and protocols come closer to optimal than any other trade exchange I’ve seen. It appears to be a developing model that is both scalable and replicable.

I will not attempt to provide here a comprehensive report or detailed analysis, rather I will highlight a few major points and provide some sources of additional information for those who are interested in doing their own research.

Some highlights:

Current membership: ~3,000

Current transaction turnover: ~1.5 million euro equivalent per month

Expected turnover for 2015: 50 million

Velocity of credit circulation: 12 times per year

Employees included as sub-accounts: 1,000

When I asked about the key factors that account for their success, here is some of what I was told:

1. Founders are dedicated to the mission to relocalize and rehumanize the economy and to reconnect people by enabling the creation of interest-free local liquidity based on the production capacity of local businesses.

2. Social solidarity and cultural cohesion, while very important and part of the mission, were NOT a pre-existing factor that would account for their early success. In fact, they have had to work hard to develop social solidarity and cooperation amongst their members, but this is now changing. One account broker told me, “I can see how behavior of many of our members has changed. When the financial crisis first began, they were starting to lay off employees or cut their wages, and they were reluctant to spend their euros. This made matters worse as the circulation of money slowed down. But as they began to participate in the process of earning and spending trade credits, they began to increase pay to their workers and to invest in their education. In one case, when a member’s shop was burglarized, other members stepped up to help by donating some of their trade credits to help their fellow member recover from the loss.”

That anecdote demonstrates the differences in behavior that results when people experience scarcity compared to when they experience abundance. In this case, the scarcity of euros caused behavior to change in the direction of reduced willingness to spend and the contraction of overall economic activity. But their experience with trade credit was much different. Realizing the greater availability of trade credits, and finding it easier to earn them, leads people to experience abundance and to be more generous and spend more liberally.

3. I was surprised to learn that the Sardex revenue model relies mainly upon initiation fees and annual membership fees (collected in euros); and that they had decided early-on to stop charging fees on transactions. For me, that approach is counter intuitive in that I have long held the view that recruitment would be most successful if membership were made easy, low cost, and risk free, and that it seems reasonable to apply the principle that users pay in proportion to the amount of services they receive. In this case, that principal would mean that those that receive more credit clearing services should pay more. Well, this may be a case where successful practice trumps rational theory. Marketing specialists should look closely at the dimensions of this phenomenon.

There is however some logic in this approach in that, since the cost of participation is relatively fixed, members should seek to maximize the benefits of their membership by trading more within the network. Initiation fees are set according to the size of the business and range from 150 to 1,000 euros. Annual membership fees are likewise based mainly on turnover and range from 350 to 2,500 euros.

4. Strong member support by an effective staff of brokers who help to arrange trades, especially for those that have high earning capacity to avoid excessive accumulation and high positive trade credit balances.

5. Recruitment strategy tries to replicate the supply chain, i.e., bring in businesses that are the suppliers of existing members or prospective members.

6. “Solidarity threshold.” Requirement that members offer their goods and services for trade credit at the same prices as their euro prices, and that payment be accepted 100% in trade credit on all transactions of less than 1,000 euros. “Blended trades,” i.e., payment in a combination of trade credits and euros are allowed on larger purchases, according to a sliding scale).

7. (a) Restrict membership to companies that have a registered office in Sardinia. This promotes social solidarity and excludes large multi-national corporations. (b) Avoid “saturation” (accepting too many members that offer the same line of products or services).

[While I am fully supportive of the former of these, and would indeed, permanently exclude multi-national companies, this latter practice of avoiding saturation I consider to be of use only in the initial stage of establishing credit clearing as a credible means of exchange and an effective source of local liquidity. Ultimately, I believe that membership must be open to any community-based small or medium enterprise (SME) that meets the basic qualifications for membership. Of course, not all of them will qualify for lines of credit.]

8. Fully compliant with reporting and tax regulations. Transparency is a matter of fundamental importance.

9. Emphasis on monetizing the unused capacity of members. Connecting unused supplies with unmet needs is a primary benefit of credit clearing services.

The Sardex company has been consulting with other groups to replicate their system in seven other regions around Italy. In the future, Sardex is planning to initiate a rebate program to bring consumers into the trading community, which will enhance the circulation of local trade credits, make Sardex better known, and stimulate more sales for their business members.

Here below is a list of a few of the many reports and sources of information about Sardex. Readers are invited to add others as comments

From an idea to a scalable working model: merging economic benefits with social values in Sardex, by Giuseppe Littera, et al, at the London School of Economic, Inaugural WINIR Conference, 11-14 September 2014, Greenwich, London, UK.

You can get a pretty good picture of the distinctive features of Sardex by viewing Giuseppe Littera’s presentation that was made (in English) at a conference in Volos, Greece, in 2014. It is to be found on YouTube at, https://youtu.be/rvaL2A8juz0

Report (in Italian) in the Italian daily newspaper, La Repubblica: Dalla Sardegna al resto d’Italia. Sardex inventa la moneta complementare. “Abbiamo ripensato l’economia.” [English translation needed.]

With social credit... see the arrow...

this is our book written in 1989 with friends about the demographic winter coming fast

Europe, l'hiver démographique

1989 - Europe

La création de l'Institut Suisse de Démographie et de Développement, ISDD, dont ... François Geinoz François de Siebenthal Michel Tricot Préface par Philippe ...World demographic winter

http://www.youtube.com/watch?

http://demographicwinter.com/

Affiliate Program

Table of Contents

1. Welcome Letter

2. Introduction-what is an affiliate program?

3. How to sign up & get started

4. Suggestions on how to get the most out of the affiliate program

Dear Affiliate,

Welcome to the Affiliate Program!

Thank you for looking at our Affiliate Program. We have designed the program to benefit

your organization – financially of course, but also by increasing traffic to your website

and by enhancing the message and image of your organization.

Your participation in the program will also serve to spread the word about Demographic

Winter: the decline of the human family. Most people are unaware of much of the

information provided by the scholars in Demographic Winter. Your active participation

in the Affiliate Program will help increase awareness about these important issues.

Please consider the extra benefits of becoming a Partner or Advocate.

Again, thank you for participating and helping to promote this important film!

Sincerely,

Barry McLerran

Producer

Introduction to the Affiliate Program

The Affiliate Program is designed to reward YOU for promoting Demographic Winter

How it works:

1. You select which promotion tool(s) (referred to in this document as “Creative’s”)

you would like to use to promote the film

a. Banner Ads

b. Trailer Links

c. Text Links

d. Invisible Codes

Add theses Tools to your website, blog, myspace, facebook, other networking sites, email

blasts, newsletters, or anywhere else you can think of—just get the word out & watch the

money come rolling in!

2. We track your referrals from those tools

3. We pay you a negotiated rate for EVERY sale that results from that referral

a. We will pay you per sale that comes as a result from your referral

For example: let’s say you add the banner ad to your site and we’ve negotiated that we

will pay you 30% for every sale that results from referrals from your site. Then, in one

month 2,000 people click on the banner ad and it leads them to our website; and 100 of

those referrals BUY a DVD, we will then pay you $6 for every one of those sales! That’s

$600, for doing virtually nothing!

SELL THE DVD as a Partner or Advocate

Give traffic to your website a boost:

The subject of demographic winter is building momentum right now, so increase traffic

to your website by doing an article on the subject, an editorial or a message from your

organization’s leader. As PR for the film and the subject increases, so will people

looking for information on the internet. Why not bring them to your site for answers

and links to the film, thus associating your organization with this important topic in their

minds.

Sell DVDs on your website:

As a Partner or Advocate you can sell DVDs on your website by:

1. Placing an ad on your website and encouraging sales

2. All sales coming from your website will be tracked

3. Your organization will earn 30% of every sale from your website – that’s $6.00

per DVD!

Buy in bulk and make more per DVD:

Your organization can buy DVDs in bulk and sell direct and:

1. Make a higher percent profit for fewer sales

2. Use for a fundraising dinner. Give a presentation, show the film, sell the film for

the $19.95 price and ask for additional donation

3. Sell them on your website for a higher profit than if we handle it

4. Buying it now will enable you to use it for a fundraiser before it goes out to the

general audience, after which they will no longer be available for fundraising

5. Use it for publicity for your organization in local media

6. Buying in bulk will get you the fundraising and PR package

7. Selling to your membership and encouraging them to buy multiple copies to give

out will help create a “buzz” around this documentary, aiding your PR, aiding the

awareness of the importance of family, aiding in a wider distribution of this

important message

Please email us for bulk order discount pricing information.

The release date for this film will be March 7.

How to Sign Up & Get Started

Now that you have an idea of what the affiliate program is and how it can benefit you

and your organization, you are ready to sign up and start earning that extra cash!

Please follow these easy instructions to get started. If at any time you have questions,

or need help with this process please call us at 1-800-896-9525.

How to get started:

1. If you haven’t done so already, fill out the Affiliate Program Application form.

a. We will review your application, and contact you if you if you have been

approved.

2. After you have been approved, you will be provided with an Affiliate login,

Affiliate ID and a password, and the link to the Affiliate Login Page (which can

also be found on the homepage).

3. Once, you have logged into the Affiliate Login Page, please check your Affiliate

Profile information, make any necessary changes. Also, please change your

password!

4. Next, select the creative’s that you would like to use to promote Demographic

Winter

a. “Images” are banner ads that you can select and use the link that the

Affiliate Generator gives you (?) to paste onto your website. (Most

popular option)

b. “Text” creative’s are text that you copy and paste onto your website, or in

a blog, an article or another place where a text link makes sense.

c. “Invisible” links are links that conceal the fact that it is indeed an affiliate

link because some merchants feel that consumers won’t click on obvious

affiliate links. But, do not worry, the invisible links still have your

individual affiliate ID information embedded in their link scripts.

* If you are in a country where English isn’t the primary language and you would like to

be a part of the affiliate program please contact us and we will work with you

individually in setting up special Creative’s for you.

5. After you have selected the creative’s-you should copy and paste the codes into

another document (see the Affiliate excel spread sheet that you can download on

the Affiliate Program webpage)

6. Give your creative affiliate codes to your webmaster and have them put the links

on your website, or wherever you desire the codes to be.

7. Next, check your Affiliate account periodically to see if it has been effective, and

that there aren’t any discrepancies.

The Payment Process

You will be paid the First Friday of every month for the previous month’s sales.

Before each payment date we will reconcile all transactions and contact you if there are

any discrepancies. Please check your account every week to stay current on your activity

level.

Please see the following section to see our suggestions on how to make the affiliate

program even more effective.

How to be more effective

Below are a few suggestions that we have found to make any affiliate program more

effective:

1. Affiliate programs work the best when the product you’re promoting is relevant to

your website. If your site is not relevant, we may still approve you to be an

affiliate, however you may not see significant benefit.

2. Banner ads (Image Creative’s) work great! However, if you have too many

banner ads on your website already, then it just becomes “noise.” We highly

suggest you limit the number of banner ads you have on your website.

3. Also, try different placements of your banner ads. If you keep the banners in the

same spot for a long time (depending upon how frequently each visitor visits your

site) they can become stagnant, reducing their effectiveness.

4. Try using multiple referral methods. Use a banner ad, and use a Text Creative to

point to www.DemographicWinter.com.

![[Europe-hiver.jpg]]()

http://demographicwinter.com/

Affiliate Program

Table of Contents

1. Welcome Letter

2. Introduction-what is an affiliate program?

3. How to sign up & get started

4. Suggestions on how to get the most out of the affiliate program

Dear Affiliate,

Welcome to the Affiliate Program!

Thank you for looking at our Affiliate Program. We have designed the program to benefit

your organization – financially of course, but also by increasing traffic to your website

and by enhancing the message and image of your organization.

Your participation in the program will also serve to spread the word about Demographic

Winter: the decline of the human family. Most people are unaware of much of the

information provided by the scholars in Demographic Winter. Your active participation

in the Affiliate Program will help increase awareness about these important issues.

Please consider the extra benefits of becoming a Partner or Advocate.

Again, thank you for participating and helping to promote this important film!

Sincerely,

Barry McLerran

Producer

Introduction to the Affiliate Program

The Affiliate Program is designed to reward YOU for promoting Demographic Winter

How it works:

1. You select which promotion tool(s) (referred to in this document as “Creative’s”)

you would like to use to promote the film

a. Banner Ads

b. Trailer Links

c. Text Links

d. Invisible Codes

Add theses Tools to your website, blog, myspace, facebook, other networking sites, email

blasts, newsletters, or anywhere else you can think of—just get the word out & watch the

money come rolling in!

2. We track your referrals from those tools

3. We pay you a negotiated rate for EVERY sale that results from that referral

a. We will pay you per sale that comes as a result from your referral

For example: let’s say you add the banner ad to your site and we’ve negotiated that we

will pay you 30% for every sale that results from referrals from your site. Then, in one

month 2,000 people click on the banner ad and it leads them to our website; and 100 of

those referrals BUY a DVD, we will then pay you $6 for every one of those sales! That’s

$600, for doing virtually nothing!

SELL THE DVD as a Partner or Advocate

Give traffic to your website a boost:

The subject of demographic winter is building momentum right now, so increase traffic

to your website by doing an article on the subject, an editorial or a message from your

organization’s leader. As PR for the film and the subject increases, so will people

looking for information on the internet. Why not bring them to your site for answers

and links to the film, thus associating your organization with this important topic in their

minds.

Sell DVDs on your website:

As a Partner or Advocate you can sell DVDs on your website by:

1. Placing an ad on your website and encouraging sales

2. All sales coming from your website will be tracked

3. Your organization will earn 30% of every sale from your website – that’s $6.00

per DVD!

Buy in bulk and make more per DVD:

Your organization can buy DVDs in bulk and sell direct and:

1. Make a higher percent profit for fewer sales

2. Use for a fundraising dinner. Give a presentation, show the film, sell the film for

the $19.95 price and ask for additional donation

3. Sell them on your website for a higher profit than if we handle it

4. Buying it now will enable you to use it for a fundraiser before it goes out to the

general audience, after which they will no longer be available for fundraising

5. Use it for publicity for your organization in local media

6. Buying in bulk will get you the fundraising and PR package

7. Selling to your membership and encouraging them to buy multiple copies to give

out will help create a “buzz” around this documentary, aiding your PR, aiding the

awareness of the importance of family, aiding in a wider distribution of this

important message

Please email us for bulk order discount pricing information.

The release date for this film will be March 7.

How to Sign Up & Get Started

Now that you have an idea of what the affiliate program is and how it can benefit you

and your organization, you are ready to sign up and start earning that extra cash!

Please follow these easy instructions to get started. If at any time you have questions,

or need help with this process please call us at 1-800-896-9525.

How to get started:

1. If you haven’t done so already, fill out the Affiliate Program Application form.

a. We will review your application, and contact you if you if you have been

approved.

2. After you have been approved, you will be provided with an Affiliate login,

Affiliate ID and a password, and the link to the Affiliate Login Page (which can

also be found on the homepage).

3. Once, you have logged into the Affiliate Login Page, please check your Affiliate

Profile information, make any necessary changes. Also, please change your

password!

4. Next, select the creative’s that you would like to use to promote Demographic

Winter

a. “Images” are banner ads that you can select and use the link that the

Affiliate Generator gives you (?) to paste onto your website. (Most

popular option)

b. “Text” creative’s are text that you copy and paste onto your website, or in

a blog, an article or another place where a text link makes sense.

c. “Invisible” links are links that conceal the fact that it is indeed an affiliate

link because some merchants feel that consumers won’t click on obvious

affiliate links. But, do not worry, the invisible links still have your

individual affiliate ID information embedded in their link scripts.

* If you are in a country where English isn’t the primary language and you would like to

be a part of the affiliate program please contact us and we will work with you

individually in setting up special Creative’s for you.

5. After you have selected the creative’s-you should copy and paste the codes into

another document (see the Affiliate excel spread sheet that you can download on

the Affiliate Program webpage)

6. Give your creative affiliate codes to your webmaster and have them put the links

on your website, or wherever you desire the codes to be.

7. Next, check your Affiliate account periodically to see if it has been effective, and

that there aren’t any discrepancies.

The Payment Process

You will be paid the First Friday of every month for the previous month’s sales.

Before each payment date we will reconcile all transactions and contact you if there are

any discrepancies. Please check your account every week to stay current on your activity

level.

Please see the following section to see our suggestions on how to make the affiliate

program even more effective.

How to be more effective

Below are a few suggestions that we have found to make any affiliate program more

effective:

1. Affiliate programs work the best when the product you’re promoting is relevant to

your website. If your site is not relevant, we may still approve you to be an

affiliate, however you may not see significant benefit.

2. Banner ads (Image Creative’s) work great! However, if you have too many

banner ads on your website already, then it just becomes “noise.” We highly

suggest you limit the number of banner ads you have on your website.

3. Also, try different placements of your banner ads. If you keep the banners in the

same spot for a long time (depending upon how frequently each visitor visits your

site) they can become stagnant, reducing their effectiveness.

4. Try using multiple referral methods. Use a banner ad, and use a Text Creative to

point to www.DemographicWinter.com.

![[Europe-hiver.jpg]](http://4.bp.blogspot.com/_9ROxT7kEIAo/ShKiYeb27HI/AAAAAAAAAIk/Bpt3SIIT55A/s1600/Europe-hiver.jpg)

Crash démographique - Wikipédia

fr.wikipedia.org/wiki/Crash_déOn appelle crash démographique, ou « hiver démographique », l'hypothèse, vérifiée en Europe (en particulier en Allemagne et en Italie) et dans plusieurs ...mographique François de Siebenthal: Démographie: Objectifs sournois du ...

desiebenthal.blogspot.com/21 sept. 2010 - Mais tout va bien, au pays de la Logique et de la Raison Pure. Le livre: " Europe: l'hiver démographique" en parlait déjà en 1989. ( Édition l'age ...2010/.../demographie- objectifs-sournois-du.h... François de Siebenthal: Démographie : la chute a commencé

desiebenthal.blogspot.com/10 juin 2009 - Le livre: " Europe: l'hiver démographique" en parlait déjà en 1989. ( Edition l'age ... nos excuses. Posted by François de Siebenthal at 08:26:00 ...2009/.../demographie-la-chute- commence.ht... activit - Famille de Siebenthal

www.de-siebenthal.com/activit.Dr Erwin Willa : Témoignage (p. 223-226). Prof. Jean de Siebenthal : Synthèse du Congrès (p. 227-229). Congrès 1989 Europe : l'hiver démographique.htm f1 f2 f3 f4 f5 - Famille de Siebenthal

www.de-siebenthal.com/ARTIC.Aeules Europe : l'hiver démographique 141 28.1.89 3. Akademiker u. Sur les droits de l'enfant 215 28.5.96 5. Algoud François-Marie Vers Dieu ou vers la Bête ?htm

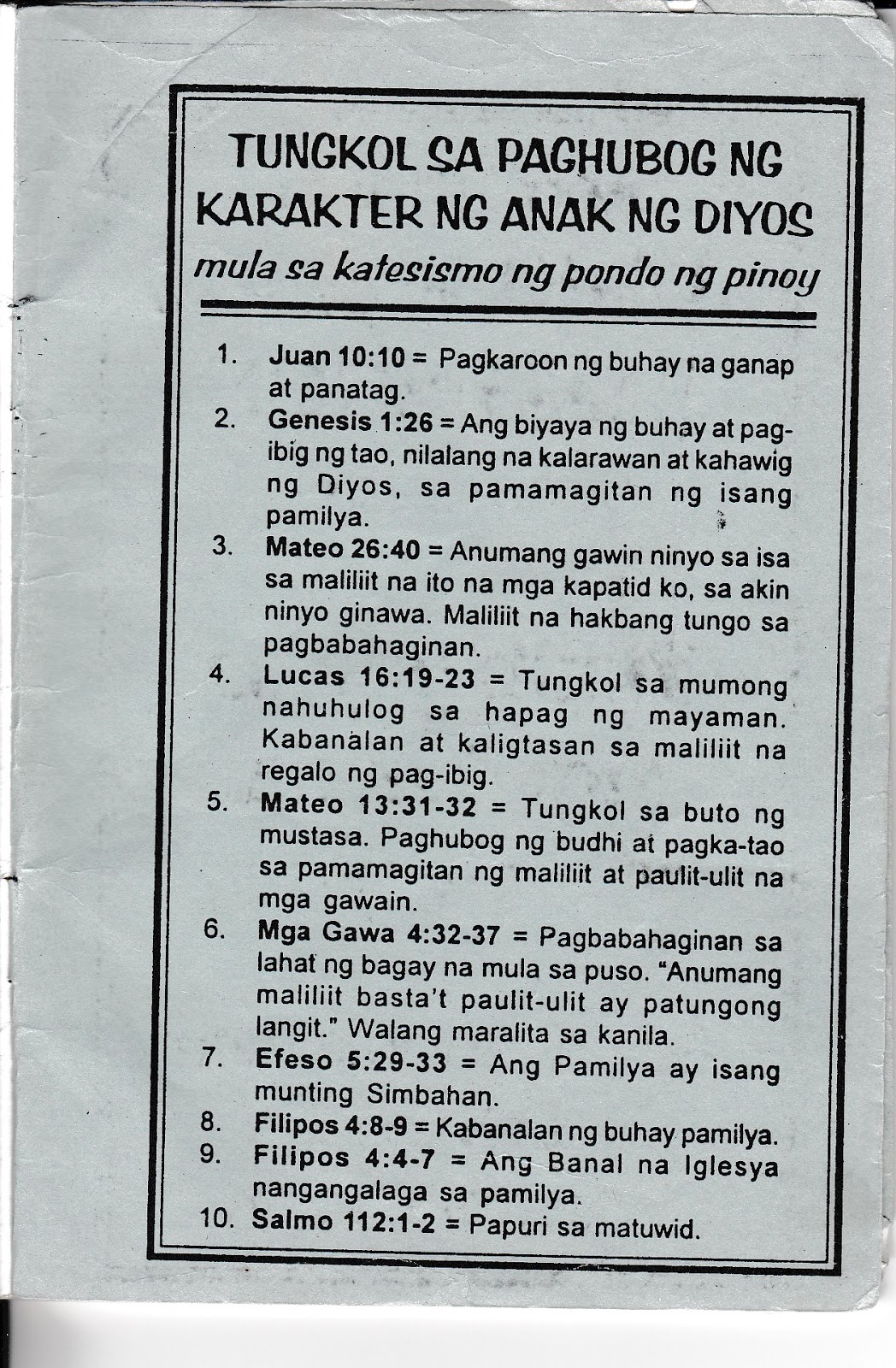

The other part is abour our work in Philippines among other countries where we got the nihil obstat & imprimatur from the Church and and Elim support among others...

2013/10/14 Bill Still <thesecretofoz@gmail.com>

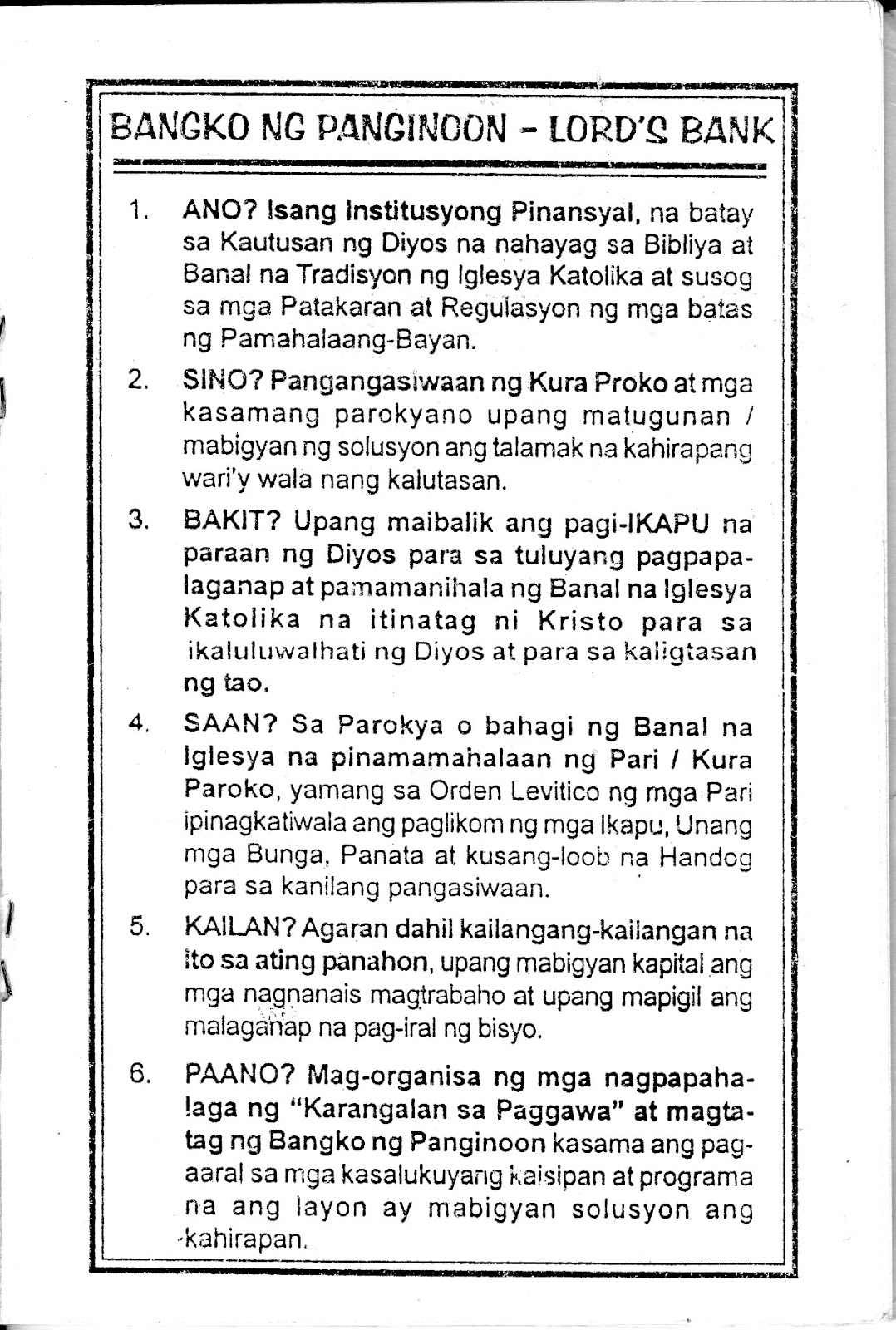

François,What is this? Someone's book?Bill StillOn Mon, Oct 14, 2013 at 3:45 AM, François de Siebenthal <siebenthal@gmail.com> wrote:nihil obstat & imprimatur and Elim...The LORDS BANKBishop Benjamin J. Bargain of Daet and Mr. Grace Economics Willy Pearl Elim Communities of Quezon City.Executive Directors: Three deacons, if possible married with many children.Auditors: Check and balance, the elders, 2 or 3, men and women.Central Monetary Authority - The Parish PriestUnder the Supervision of the Diocesan BishopGuided by God's Laws, the Canon Law,the Govemment LawsAnd the Diocesan Decrees and Statutes

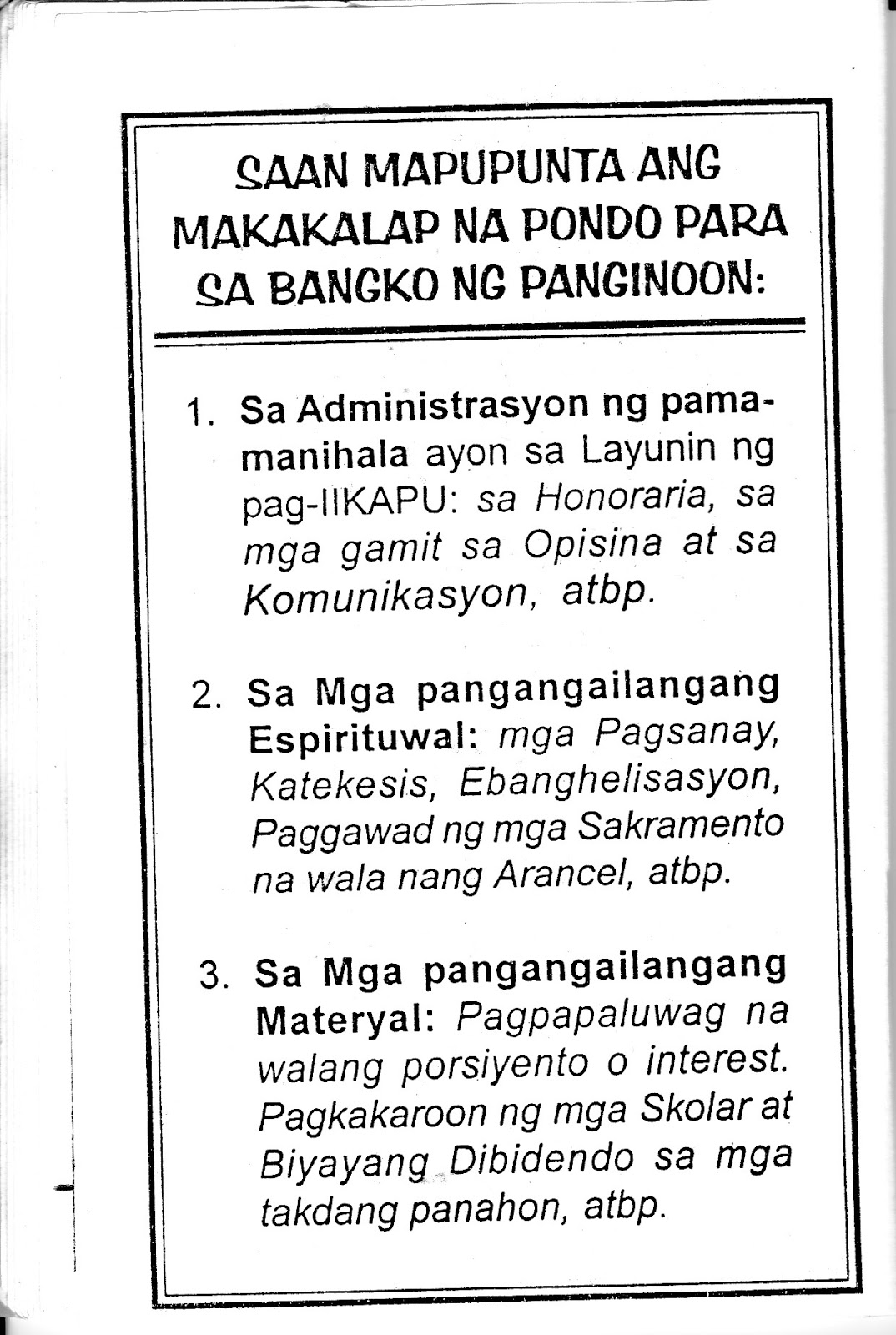

Material Infra-GHQ Wo inierest Nor penaky Village For Offices Centers & Immovable Scholarship Acquisition Construction Sharing of Maintenance Mass Media

- Changes from the old methods... the success of banking.

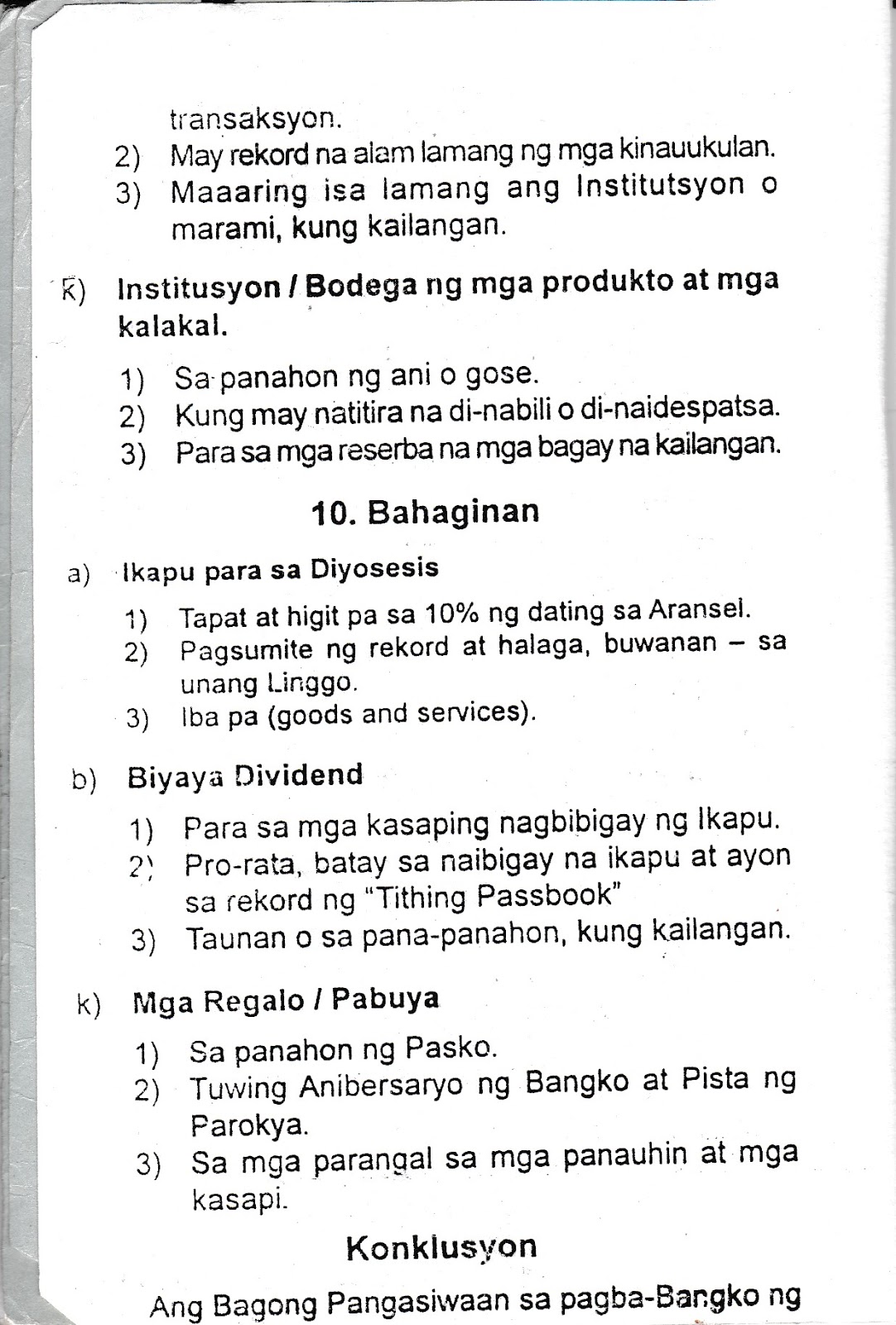

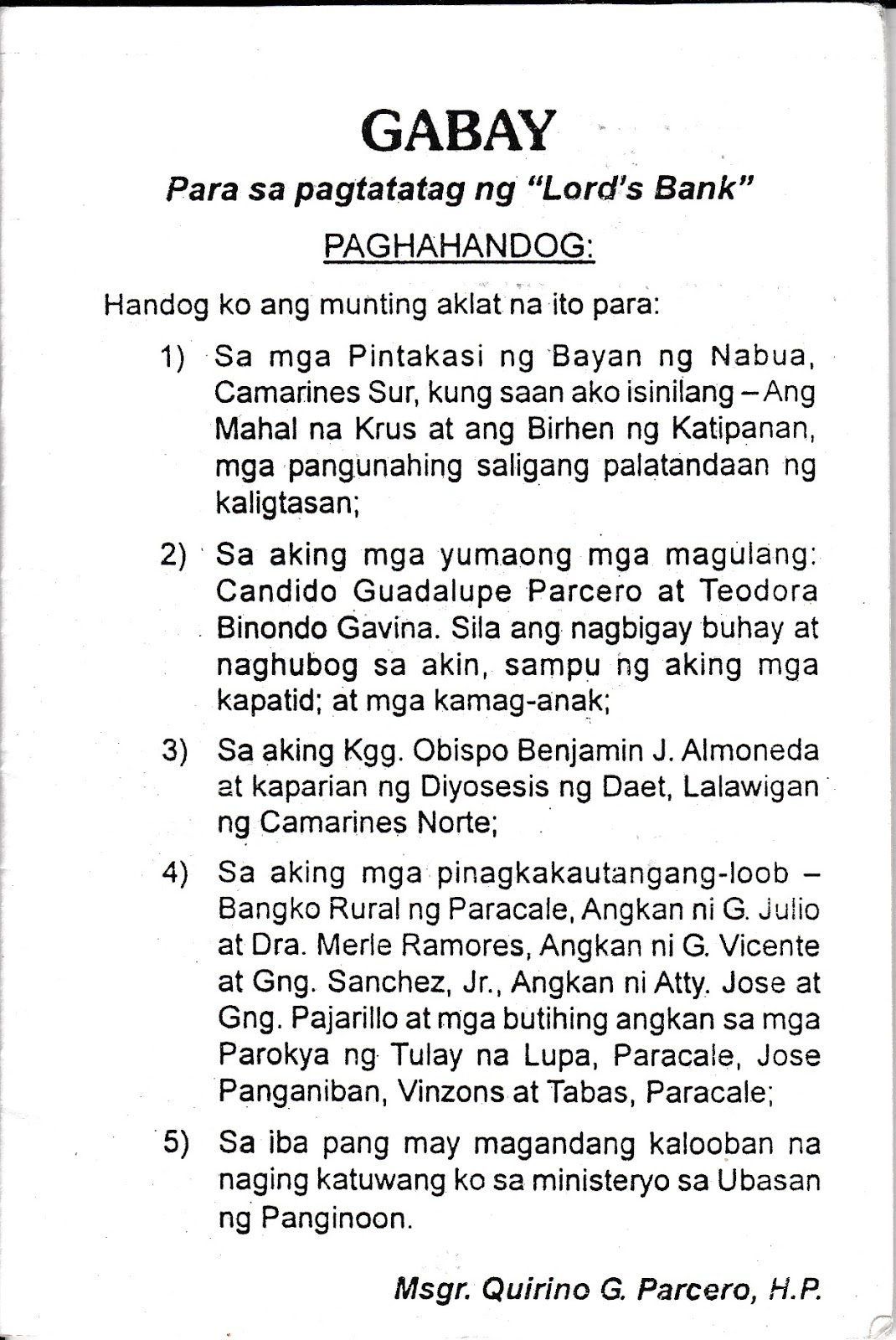

To help the needy et non-members can supply the desired items on ... and dreams in life....GUIDEFor the establishment of the "Lord's Bank"Offerings:I am offering this booklet to:

- In the patron of the Municipality of Nabua, Camannes Sur, where I was born, The Beloved Cross and the Virgin Katipanan, basic basic safety signs;

- In my late parents: Candido et Teodora Guadalupe Parcero Binondo Gavina. They gave me life and naghubog, together with my brothers and relatives ...

- In my Hon. Bishop Benjamin J. Almoneda and clergy of the Diocese of Daet, province 'of Camarines Norte;.

- In my ...Rural Bank of Paracale, Mr. Clan Julio and Dra. Merle Ramores, Mr. Clan Vicente and Mrs. Sanchez, Jr.., The Children's Atty. Joseph and Mrs. Pajarillo and wonderful families in the Parish. Flyover Land, Paracale, Jose Panganiban, Vinons and Contour, Paracale;

Msgr. Quirino CI Parcero, HP

- In Other magnanimous I became partners in ministry to the Lord's Vineyard.

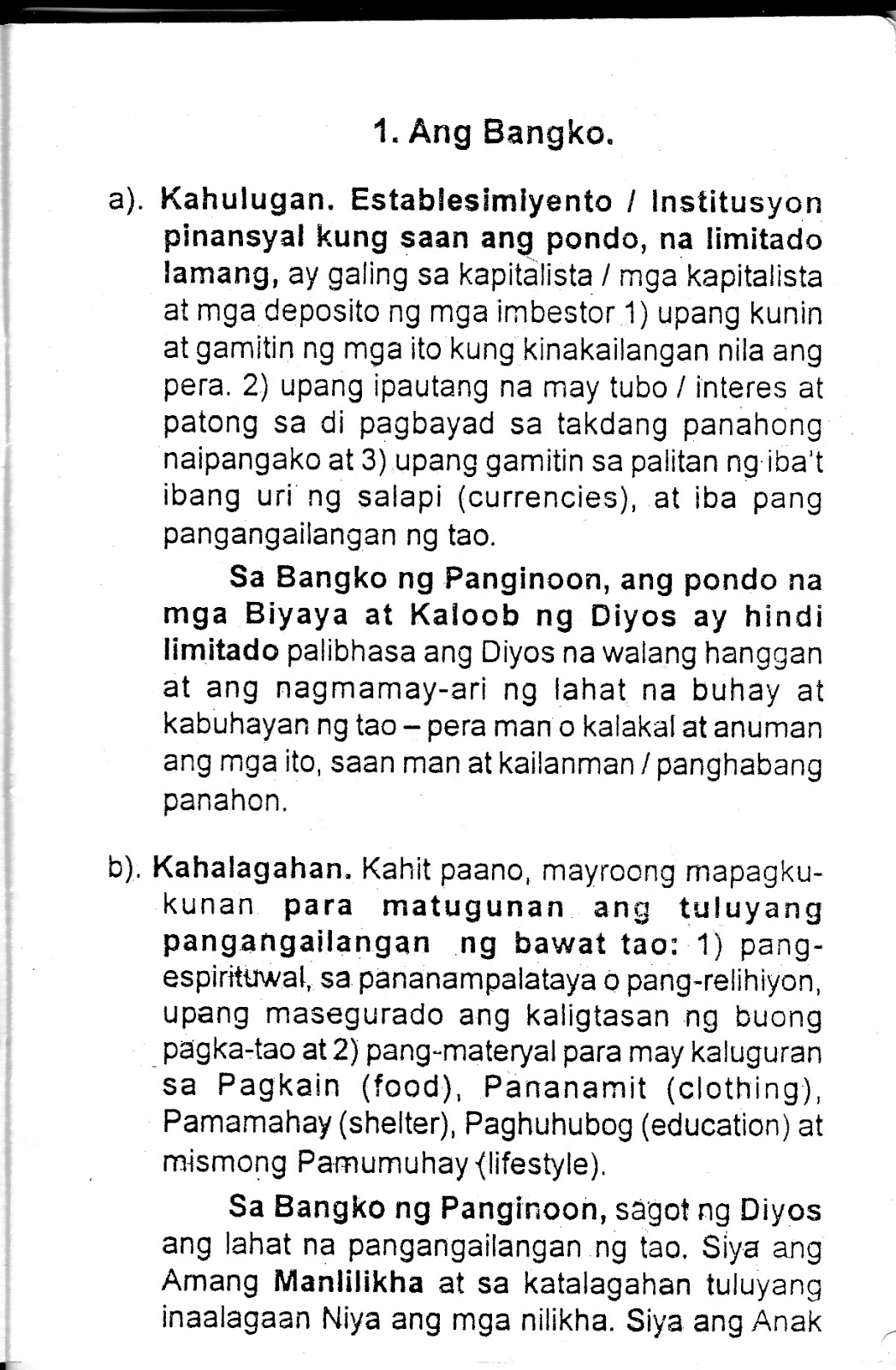

- Definitions. ...funds, limited only, from the investor / investor and the investor deposits 1) to extract and use them if they need the money. 2) to be loaned with profit / interest and coating the non payment of promised time frame and 3) to be used to exchange different types of currency (currencies), and other human needs.

Bank of the Lord, and funds the gift of God's grace is not limited Being the eternal God and owns all the lives and livelihoods of people - money or...and whatever they are, wherever and never / forever.

- Importance .. Kahn how, there are resources to meet each person eventually ...a delight for Food (food ), Clothing (clothing), Housing (sheftr) Moulding (education) and its Lifestyle Olfestyle).

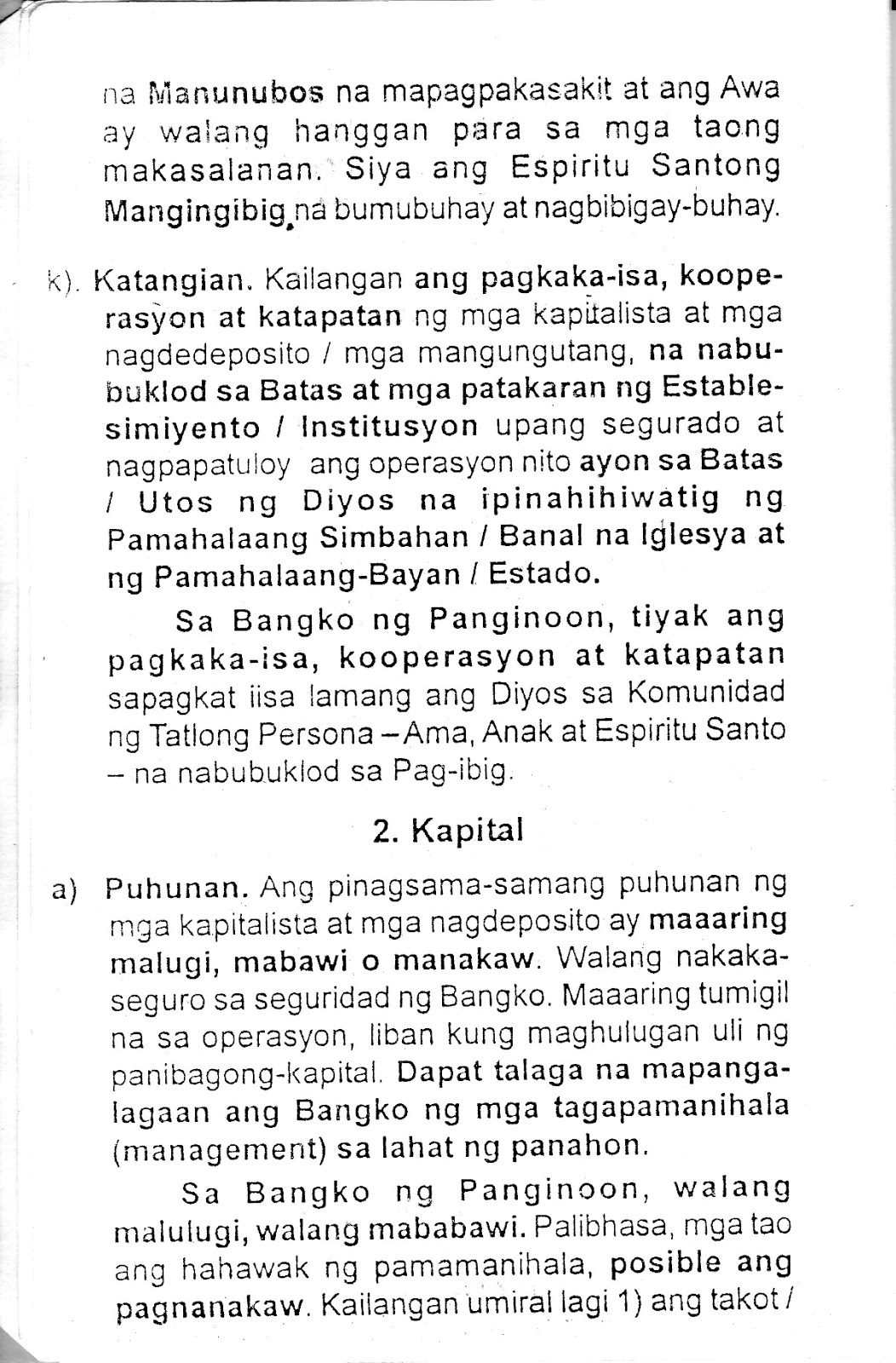

Bank of the Lord, God answers all human needs. He is the Creator and Father eventually cared nature He created. He is the SonRedeemer that sacrificing and Mercy are endless for the devil. He is the Holy Ghost Lover that raises and gives life.k). Properties. Need unity, cooperation and loyalty of ... / the debtor, who sealed the Act and the rules .../ Institution to be assured and continuing its operations in accordance with the Law / Commandment Church suggestive of Government / Holy lèlesya and Government-Town 1 State.Bank of the Lord, surely the unity, cooperation and honesty because there is only one God in the Trinity Community, Father, Son and Holy Spirit - which sealed the love.2. Kapitaia) Investment. The aggregate turnover of ...and deposits may sink, or recover stolen. No security ...Bank. Operation may be stopped, unless renewed, again ...capital. You should really protect the Bank of superintendent (management) at all times.Bank of the Lord, not suffer loss, no recovered. Being, the people doing the supervision, possible theft. ...devotion to the Lord just 2) sils serve not only as servants, but servants may actually lbig, so 3) always ana the Lord for all the work and things, to think only in the glory of God and the salvation of man , and not the pers, honor or pleasure purposes.

- .... And if it has planned to build. the shelter of the guard in the field? ... and estimate the inheritance ... Luke 14:28. You should only estimate the Halage of Finance destined for the need ... in time, in different ways and play. Should not neglect the need of the people involved in the exercise.

- Financial auditing. Required ... approved and the Auditor Evaluation of record entered (income) and ... (expenses) on a daily, monthly and annual. ... audit for running and employees; inventory of all its transactions and equipment / instruments.

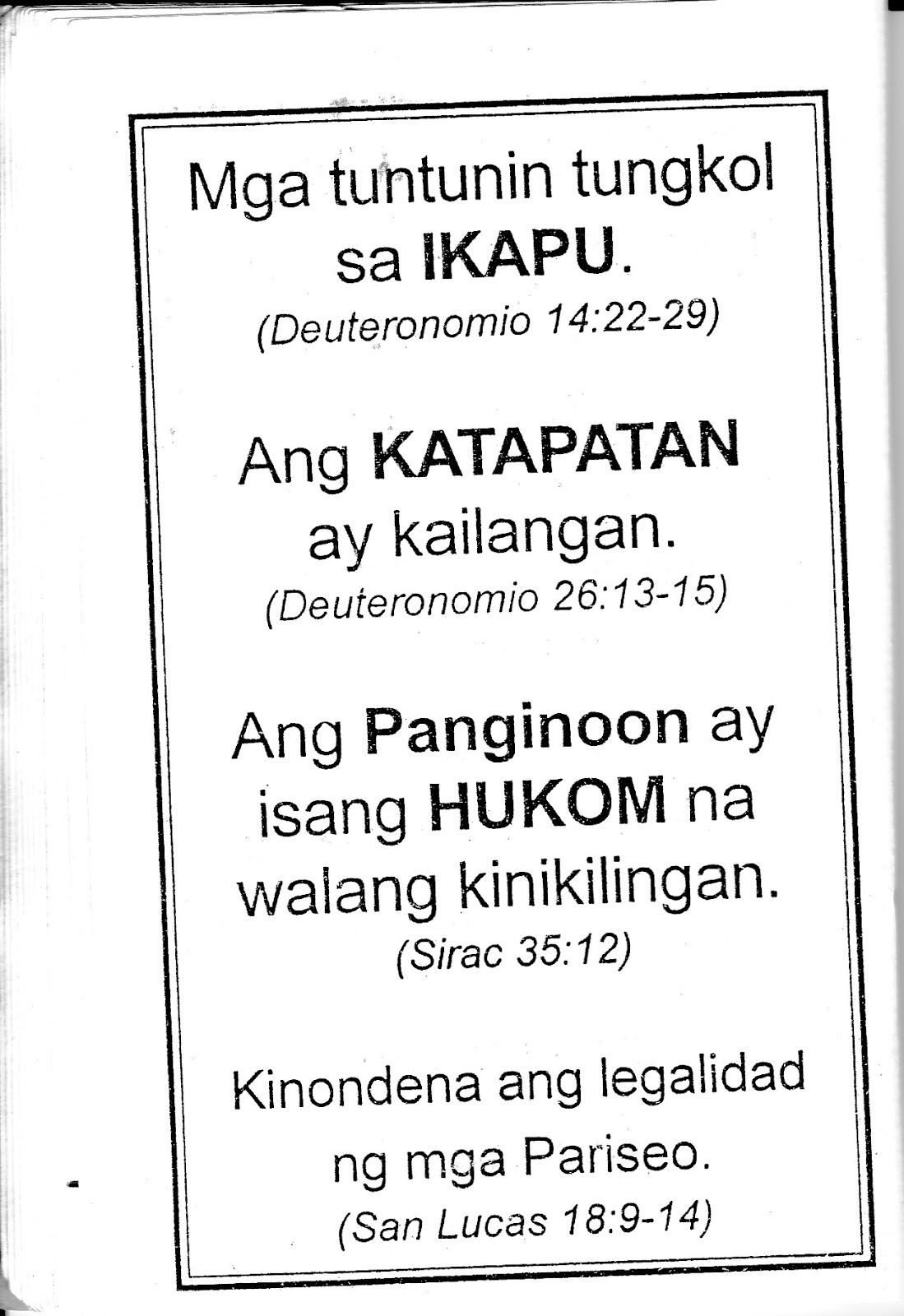

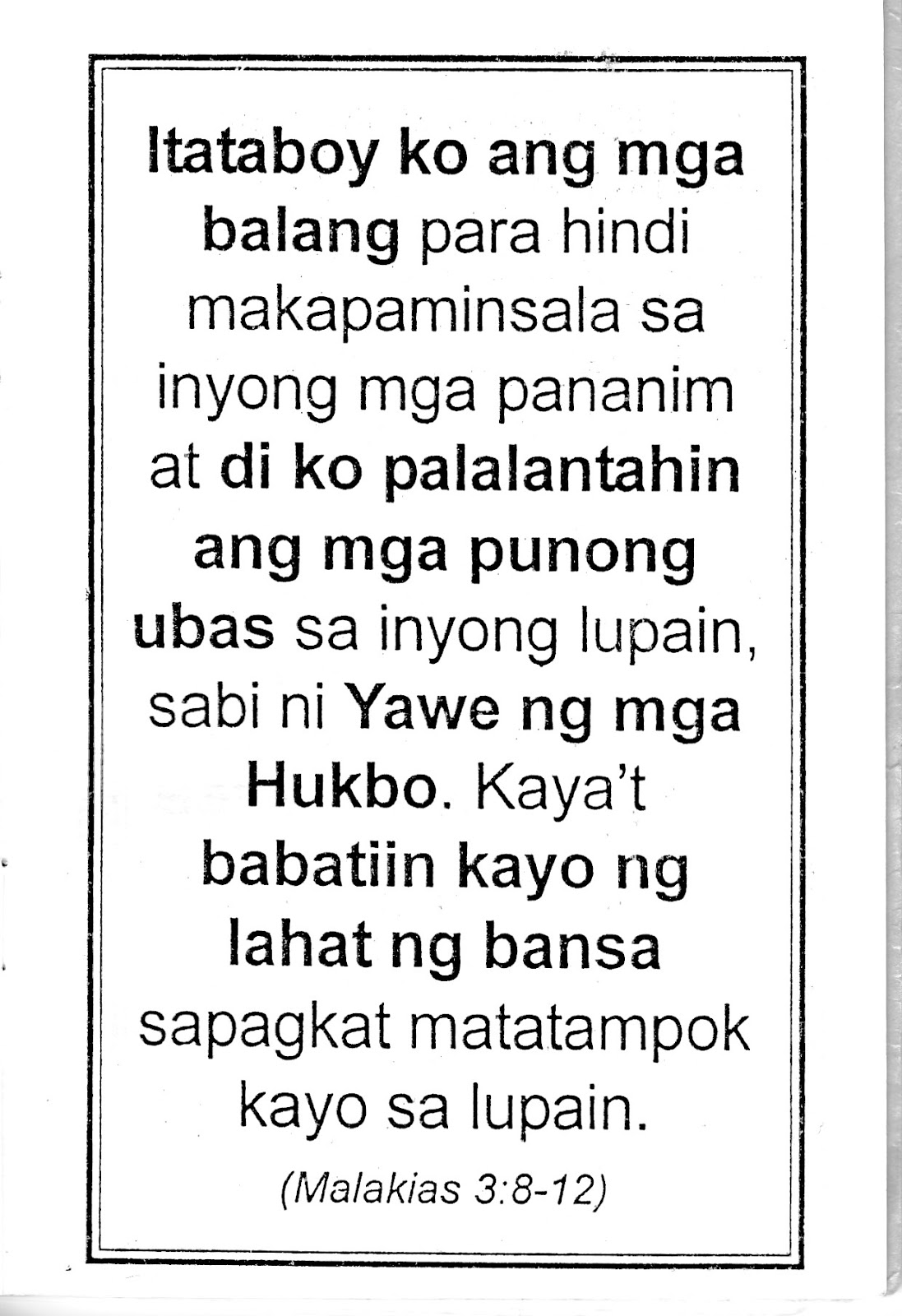

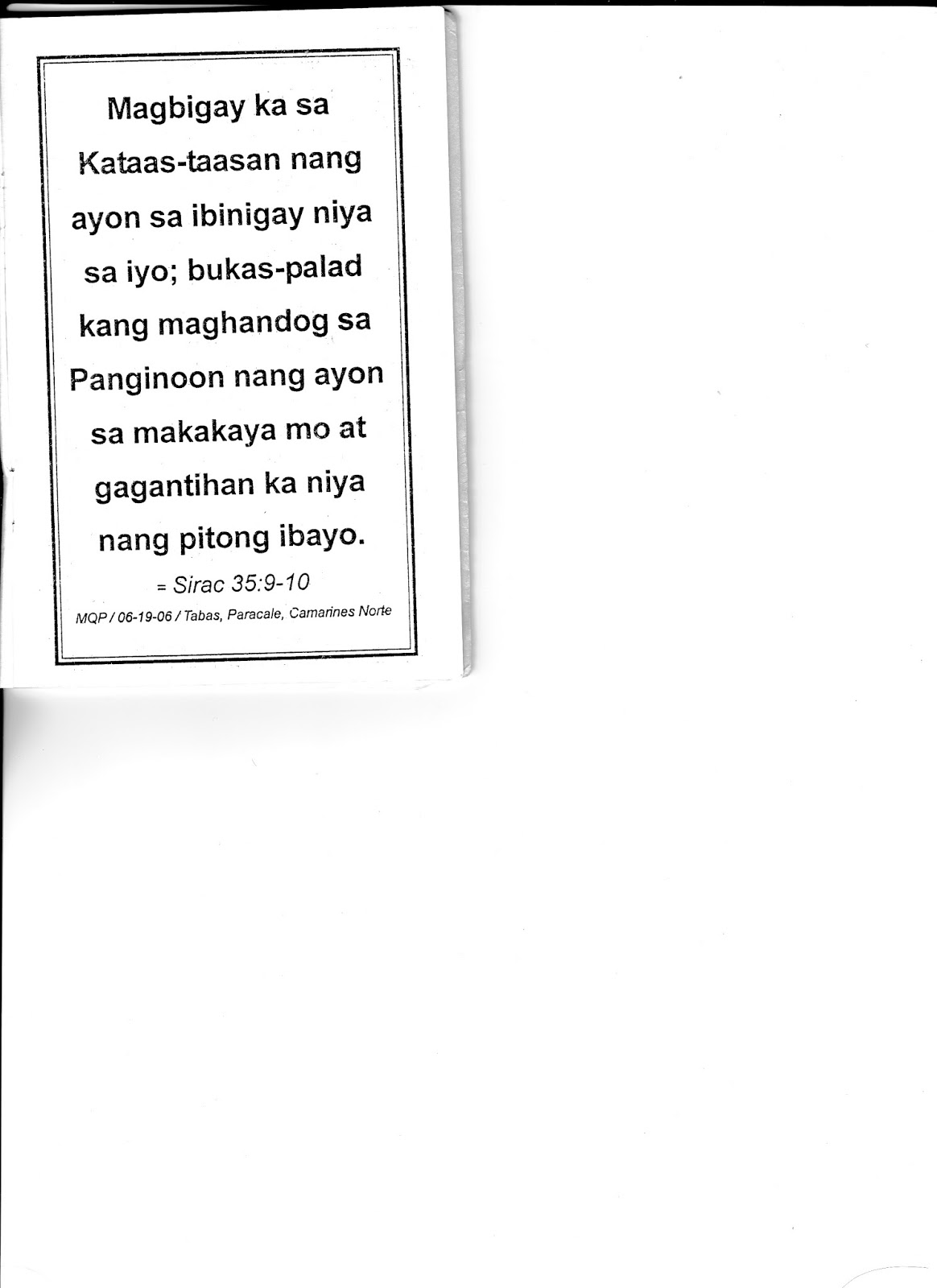

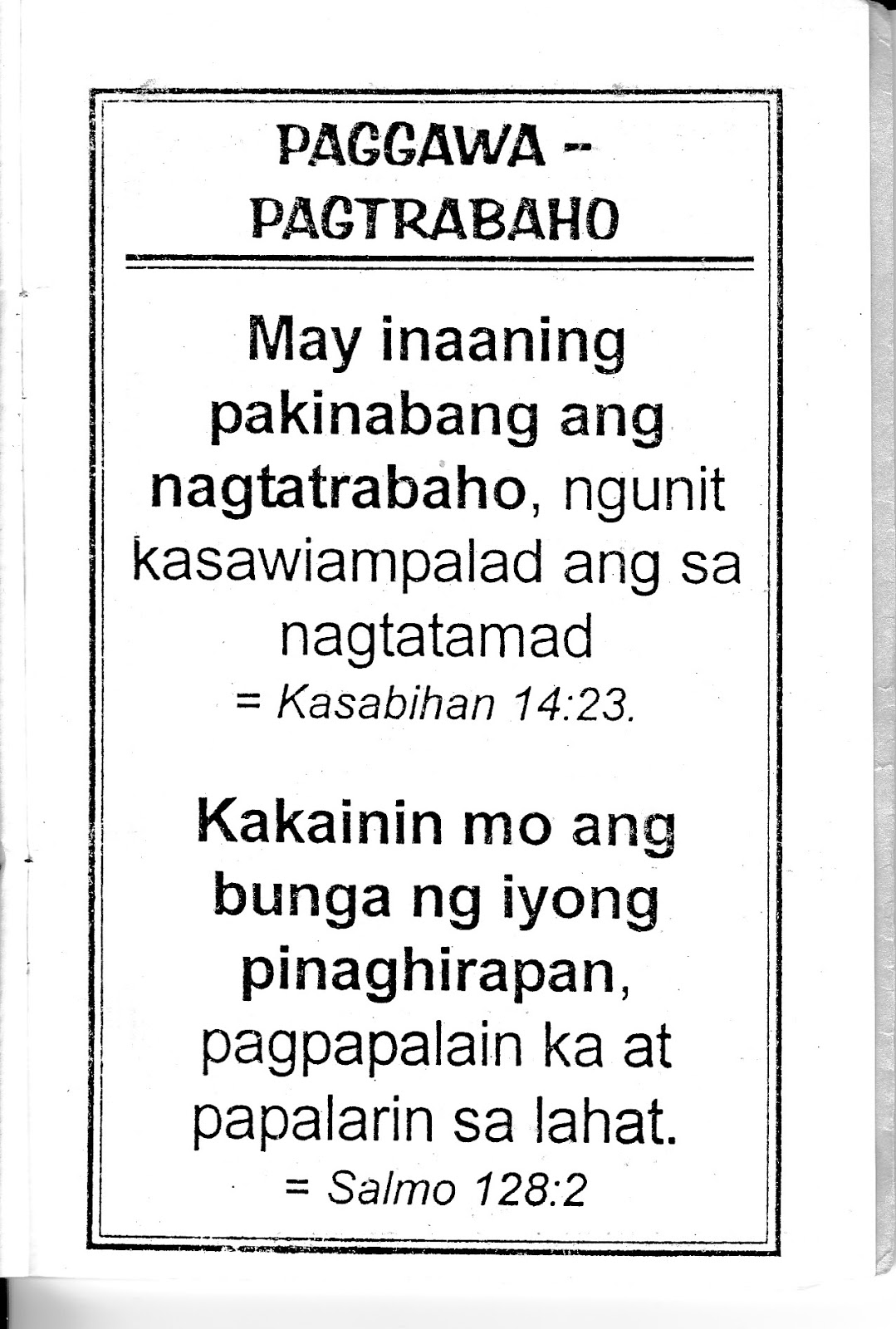

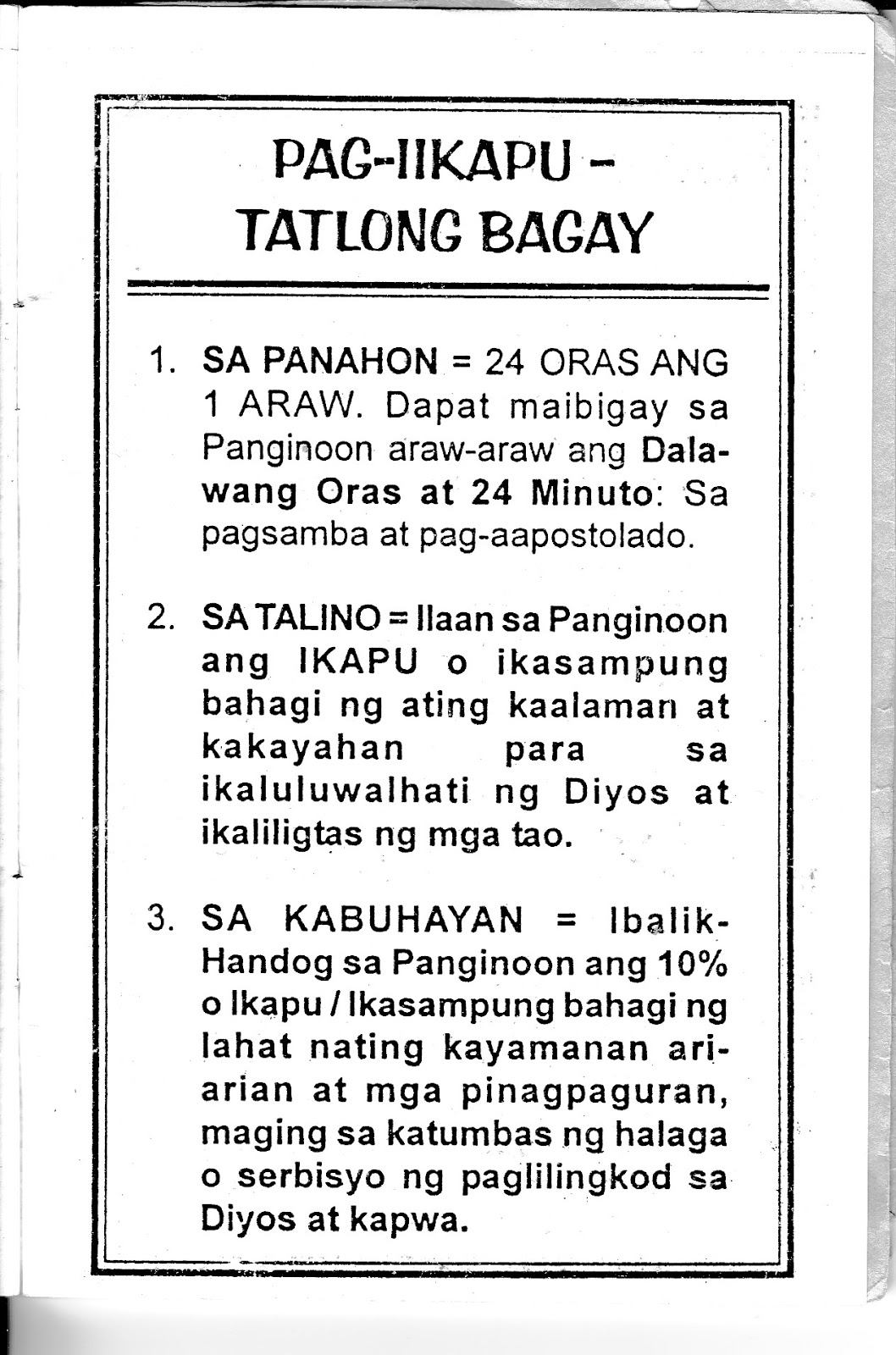

3. lkapu.The Tithing is one-tenth (1/10) of any grace and gift of God to every man for the Lord. Leviticus 27:30-33. Patient love and kindness. 1 Corinthians 13:4.Provided the Levites Meeting Tent. Numbers 18:21-29. .... Deuteronomlo 12 à 0.8 to 9, in priest Aaron. Numbers 18:28 best. 18:29 ET Numbers Hebrew priest Melkisedek 7:11-8.Malachi 3:7-12 promised identified Jews Nehemias 13:5,12.Give as you ibihlgay him. Sirat 35:9. So give ... according to him, not unhappy ...; love of God nagbiblgay welcome. God is able to enrich you in all things so you do not want to even mention and multiply as your charity. 2 Corinthians 9:7-8. Give, and you will receive an abundance measure, packed together, shaken and overflowing pour into your bosom. Sépagkot sutukatin you scale you use. Luke 6:38. ...giving more blessed than receiving. Acts 20:35.The sows little will reap little, and sowed much to g's a plenty. 2 Corinthians 9:8.Terms Deuteronomy 14:22-29. Loyalty ...26:13 -15. The Lord is a neutral judge Sirat 36:12. Tobias kept 1:6-9 condemned the legality of the Pharisees Luke 18:9-14.a) Life. ... All life and all human life from God. Tithing is only asking for the Lord.

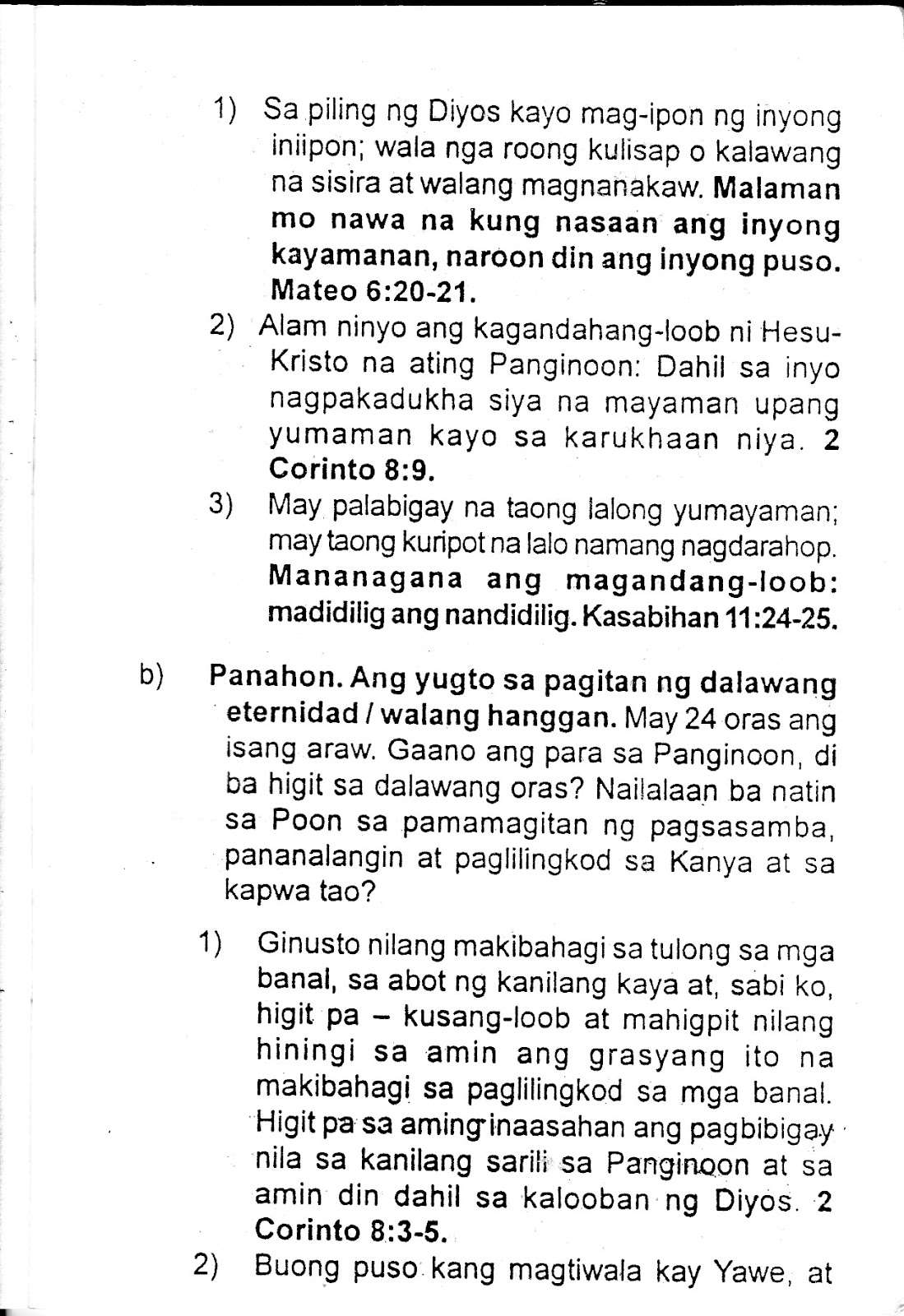

- In the presence of God you lay your collected; ...was there with insecticide or no rust destroy and thieves. You may already know where your treasure is, there will your heart. Matthew 6:20-21.

- You know the grace of our Lord Jesus Christ: As you nagpakadukha he rich to wealthy enjoy his misery. 2 Corinthians 8:9.

- Large-hearted people may be more wealthier; person may turn stingy especially poverty. This is kind abound: watered the nandidilig. Proverbs 11:24-25.

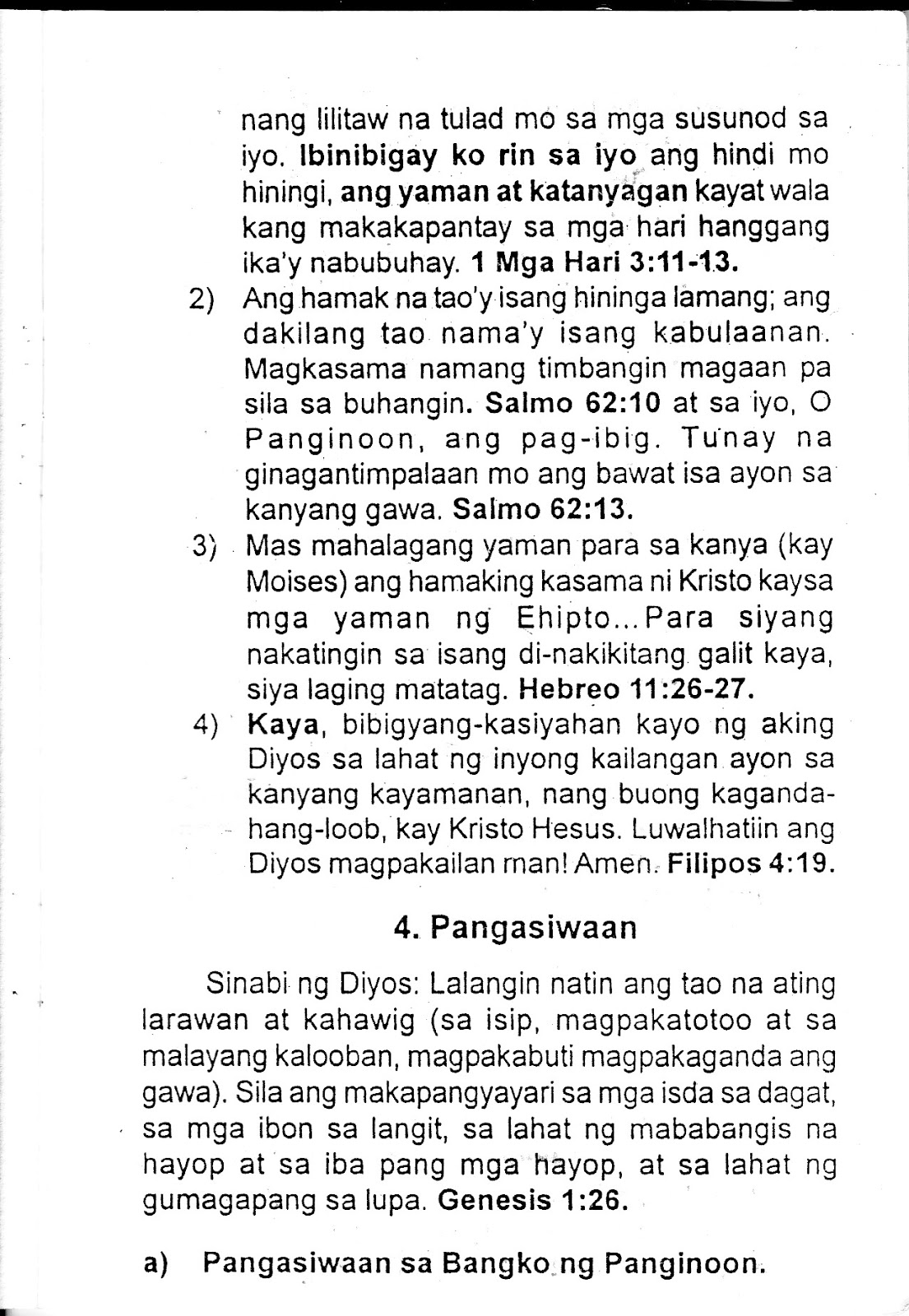

b) Period. The period between the first two eternity forever. May 24 hours a day. How much for the Lord, are not more than two hours? Do Nailalaan Poon patin sa sa parriamagitan of worship, prayer and service to Him and to fellow human beings?

- They wanted to share to help with the saints, for Aboi they can and, I said, more - strictly voluntary and they asked us to share the blessings of the divine service. More PE aminginaasahan they giving themselves to us Pangimon and also because the will of God. 2 Corinthians 8. :3-5.

- Sincerely can trust Yahweh, ..

Do not hang on own thoughts. Remember him in all your ways .... Proverbs 3:5-6.3) To whom I work and depriving myself of pleasure? It may be no significance and bad business.C) Brains. Conform to the ant ... he stores food in the summer, gathering live in during the summer ... Proverbs 6:6-8. Six things Yahweh hates, seven are an abomination in his will : 1) haughty eyes 2) tongue liar 3) hand ...innocent blood 4) rogue scoundrel 5) feet go quickly to evil 6) False witness and 7) who sows discord among brothers. Proverbs 6: 16-19. Yahweh gives wisdom, his mouth come knowledge and understanding. Proverbs 2:6.1) Because it's your hlnlllng and not long life or wealth for yourself, or death of your enemies, ...prompts you to decide to ..., I grant you ....My comments:Bad translations from Rome.Example in the recent papal encyclical Caritas in Veritate...

Pawnbroking is not monte di pietà...Can we translate the concept hospital by bordel or brothel or whorehouse?65. … Furthermore, the experience of micro-finance, which has its roots in the thinking and activity of the civil humanists — I am thinking especially of the birth of pawnbroking — should be strengthened and fine-tuned. This is all the more necessary in these days when financial difficulties can become severe for many of the more vulnerable sectors of the population, who should be protected from the risk of usury and from despair. The weakest members of society should be helped to defend themselves against usury, just as poor peoples should be helped to derive real benefit from micro-credit, in order to discourage the exploitation that is possible in these two areas. Since rich countries are also experiencing new forms of poverty, micro-finance can give practical assistance by launching new initiatives and opening up new sectors for the benefit of the weaker elements in society, even at a time of general economic downturn.Real translation and its importance:A mount of piety is an institutional pawnbroker run as a charity in Europe from the later Middle Ages times to the 20th century, more often referred to in English by the relevant local term, such as monte di pietà (Italian), mont de piété (French), or monte de piedad (Spanish).In Switzerland, e.g. the cantons of Bern and Zürich enacted elaborate laws for the regulation of the business. In Zürich the broker must be licensed by the cantonal government, and the permit can be refused only when the applicant is known to be a person underserving of confidence. Regular books have to be kept, which must be at all times open to the inspection of the police, and not more than 1% interest per month may be charged, just to cover the costs and not for profits, as asked by the Church, i.e. permitted by Medici Pope Leo X’s usury-for-a-good-cause: the Monte di pieta, so-called “charity banks” operated in the Renaissance in the name of the poor, with no profits. A loan runs for six months, and unredeemed pledges may be sold by auction a month after the expiration of the fixed period, and then the sale must take place in the parish in which the article was pledged. No more than two persons at a time have ever been licensed under this law, the business being unprofitable owing to the low rate of interest. In the canton of Bern there were once two pawnbrokers. One died and the other put up his shutters. The Zürich cantonal bank, however, conducts a pawnbroking department, which lends nothing under 4s. or over £40 without the special sanction of the bank commission. Loans must not exceed two-thirds of the trade value of the pledge, but 80% may be lent upon the intrinsic value of gold and silver articles. The swiss establishments make practically no profit.Fribourg in Switzerland and Rerum Novarum,3...The mischief has been increased by rapacious usury, which, although more than once condemned by the Church, is nevertheless, under a different guise, but with like injustice, still practiced by covetous and grasping men....

Elim Communities—History

On September 28, 1980, Sis Luli Nakar received a spiritual revelation. The late Fr ...2009 Elim Communities • Springs Foundation Inc. • All Rights Reserved.Elim Communities—Articles

by Bro Willy Nakar. Have you ever fallen in love? Discover a ... Events | Store | Contact. © 2009 Elim Communities • Springs Foundation Inc. • All Rights Reserved.Elim Communities—Store

You Can Be Healed by Willy Nakar ... The Beauty of Prayer by Didi Nakar Marañon ...Enjoy relaxing melodies of well-loved Elim songs and new instrumental ...Elim Communities—Elim Missions

In the year 2000, Presiding Elder Bro Willy Nakar and Keeper of the Vision Sis LuliNakar shared a new direction for Elim, as inspired by Isaiah 54:2-3: Enlarge ...Vix Pervenit , addressed to the Bishops of Italy, about contracts, and in which usury, or money-lending at interest, is clearly condemned. On July 29, 1836, Pope Gregory XVI extended this encyclical to the whole Church. It says:“The kind of sin called usury, which lies in the loan, consists in the fact that someone, using as an excuse the loan itself — which by nature requires one to give back only as much as one has received — demands to receive more than is due to him, and consequently maintains that, besides the capital, a profit is due to him, because of the loan itself. It is for this reason that any profit of this kind that exceeds the capital is illicit and usurious.“And in order not to bring upon oneself this infamous note, it would be useless to say that this profit is not excessive but moderate; that it is not large, but small... For the object of the law of lending is necessarily the equality between what is lent and what is given back... Consequently, if someone receives more than he lent, he is bound in commutative justice to restitution...”The interest in one of the factors that triggers inflation, and not the opposite. Pope John Paul II's encyclical letter Veritatis Splendor reminds us that there are intrinsic evils and absolute sins. To ignore them may suppress personal sin (according to St. Thomas Aquinas, the borrower commits no sin), but society pays for this misdeed, even at the cost of its own disappearance, and those who favor the ignorance of the sin of usury are responsible for endangering the survival of the population.What comforts us, however, is that this condemnation of usury is repeated in the new Catechism of the Catholic Church, at the end of the comments on the Seventh Commandment.Impossible contracts are nullIt is impossible to pay back interest-bearing loans, either they are compound or not. Take the following example: Croesus borrows a principal of 100 at the birth of Christ. If one applies an interest rate of 10%, the sum to be paid back in the year 2000 is (100 x 1,12000), or six times ten to the power of eighty-four, or a number with 84 zeros, which simply blows the mind... It would represent 10 to the power of 68 houses for every person on earth. It is obvious that it is impossible to respect such a contract.A French mathematician, M. Levy, showed that, after a while, all the wealth in the world will be owned by the banks, through the simple application of mathematical rules.Money is a human creation which, if the interest is admitted, begets more money. This money is not only a sign; it really causes deaths and injuries, in every area. It is more prudent to forbid any new organism that is self-reproducing (like viruses, the development of new species in vitro, etc.), including abstract concepts like money that have consequences in real life. The common good called “money” is in the hands of people without scruples. It is a duty for society to take back control over the issuance of money.It is said that everything has a cost, and so the interest would be the cost of money. However, money is not a thing, a commodity, but a sign, a common good that belongs to all, just like water or air. It is precisely the dream of the greedy to make people pay for the air and water they consume. Money is a universal, and to leave its creation into the hands of the supporters of death is a crime.Today, money is more and more invested in labor-saving technology rather than in creating jobs. The interest causes the repayment of loans to the banks to go before the wages of workers, and to prefer to lay off these workers instead of paying them. This is how human rights work today: money, a sign or abstraction, comes before the human person, a reality. Where is the dignity of the fathers of families, who are not bankers? Besides, bankers do not have large families, for money comes even before their own children.Abortion: a sacrifice to MolochThis swindle of the “creation” of money by the banks, and the widespread use of interest on the loan of money, favor economic crises and abortion when loans have to be paid back. In Switzerland, the first reason given by women who had an abortion is the repayment of loans, contracted by themselves or their families. We know that there are other reasons (hedonism, selfishness, fashions, social pressure, frivolity, ignorance, etc.), but to shut up our eyes and do nothing against one of the causes is neither scientific nor Christian. To let the people who earn money without working (by collecting the interest on their loans) crush the poor who are defenseless, is ridiculous. However, to defend the poor is far from being ridiculous.History of ancient Egypt shows the close link between mortgage rates and the decline, even disappearance, of the population. (See the analysis of Belgian historian Pirenne on the 20% rates that caused the deadly exposition of children to the sun.)The new Catechism of the Catholic Church maintains the condemnation of interest and its harmful role at the end of the comments on the 7th Commandment, which forbids to steal. As lay people, we must make this condemnation understood by all, for it is a liberation for the poor; moreover, an economy based on investment in real developments and improvements (and not simply hoarding money through the gimmick of the interest rates), is much more dynamic, and favors a reduction of prices, while rewarding those who take risks in investing in new developments.Justice is necessary to achieve holiness. It is too easy to wash one's hands of the matter by saying that one understands nothing in economics. Economics is not so complicated, especially when one takes the trouble to humbly study solutions that are finally more practical than those who manipulate public opinion want to make you believe.For many centuries, the Church has been suffering, because her sons are prisoners of a huge disinformation campaign. Maurice Allais, 1988 Nobel Prize winner in Economics, wrote that the present international financial system is the biggest disinformation system in human history. The sons of darkness control this disinformation and crush the weak, often with the help of the ignorant of good faith. Let us unmask them, to give some fresh air amidst this general atmosphere of corruption.What to do?Why not react now? The human race has survived for centuries without this so-called creation of money at interest by banks, and even with no banks at all. So, why not abandon these inhuman and outrageous interest rates that know no limits and steal time from us as educators of our children? The interest is time stolen from fathers and mothers.Nations spend billions for research in physics. Let us spend a few million to study more carefully the social doctrine of the Church and the practical solutions it entails in favor of a sound economy. Let us create a center of studies and formation for social action.Let us make the promise made to Abraham possible. The earth is huge and generous, as well as the seas. All the serious experts, after long studies (cf. Julius Simon), admit that our planet can feed all the population to come in the future. In fact, those who believe that the earth is overpopulated neither believe in God nor in His promise. Let us learn again to utter this greeting of the sons of Abraham: pax, peace, shalom, salam... This peace, as Blessed Mother Teresa of Calcutta said, will come on earth only if abortions are stopped, and if we accept those who are different, the disabled.A salary for housewivesHousewives, mothers who stay at home, work just as hard as those who are hired in the workforce. They deserve a real salary, which will create more job opportunities, boost consumption and the economy, and allow the Gross National Product to double. It was possible to finance two world wars, so there is no reason why it would not be possible to finance this wage to housewives. In Canada, it is estimated that the work of housewives represents 46% of the GNP. So it is simple justice, as Pope John Paul II said, to reward them with a salary.Is is true that:The less the children in a family, the less vocations to sharing and generosity?The best school to teach the principle of subsidiarity is a large family?The main flaw in world politics is this generosity in the existence of intermediary bodies?The contraception mentality is directly aimed against large families?The system of interest directly attacks the family?The interest is a theft of time and children?The creation of money through interest is a lie and a swindle, a theft to the detriment of future generations (unborn children)?Can any person of good will take part in this slaughter, by action or omission? Can we stand up and stop this mechanism?Is the teaching of St. Thomas Aquinas on usury still valid today? Can the time that belongs to God be stolen? This is a good explanation for stress.Any human invention that has no limits is monstrous; the system of interest rates has no limits. Moreover, a means of exchange, or unit of measurement, cannot multiply by itself. If money breeds more money today, it is at the expense of our own children. This is criminal!It is easy to show that the present crisis is in large part due to this search for zero population growth, based on flawed facts and analysis. What a mistake it is to think that the earth cannot support all of the present population, whereas Europe alone could feed many times the world's population, not to mention the resources of the oceans that are barely developed.For those who say: “We will have to change the way our deposits are managed in banks,” I reply: “This is true, and you will be rewarded a hundredfold, for a dynamic economy will benefit all, unless your selfishness make you sad to see others happy. How sad it would be it you were in such a situation, especially since you risk eternal damnation.All this work is done with the hope that a few simple economic concepts can be explained for the good of the poor, the unborn, especially in Third-World countries. Don't believe those who complicate everything to keep their control over the economy, for billions of human beings will never be born because of this control. True love cannot accept interest, but it can accept just profit. Let us entrust the future of mankind to the family, with mothers having for their model, Mary.François de Siebenthal

system as identical to the creation of money by “counterfeiters,”

the only difference being that those who profit are different.

He proposed, therefore, that although all banks would be

private, except for the Central Bank, all income derived by the

Central Bank’s creation of money should be returned to the

State, enabling the latter, under present circumstances, to do

away with practically the whole of the progressive tax on income.

This would eliminate the present circumstance where profits

and their beneficiaries are not transparent. Such revenues, he

wrote, “merely generate inflation, and by encouraging investments

that are not really profitable for the community...

The Wall Street Pentagon Papers: Biggest Scam In World History Exposed – Are The Federal Reserve’s Crimes Too Big To Comprehend ?

What if the greatest scam ever perpetrated was blatantly exposed, and the US media didn’t cover it? Does that mean the scam could keep going? That’s what we are about to find out.

I understand the importance of the new WikiLeaks documents. However, we must not let them distract us from the new information the Federal Reserve was forced to release. Even if WikiLeaks reveals documents from inside a large American bank, as huge as that could be, it will most likely pale in comparison to what we just found out from the one-time peek we got into the inner-workings of the Federal Reserve. This is the Wall Street equivalent of the Pentagon Papers.

I’ve written many reports detailing the crimes of Wall Street during this crisis. The level of fraud, from top to bottom, has been staggering. The lack of accountability and the complete disregard for the rule of law have made me and many of my colleagues extremely cynical and jaded when it comes to new evidence to pile on top of the mountain that we have already gathered. But we must not let our cynicism cloud our vision on the details within this new information.

Just when I thought the banksters couldn’t possibly shock me anymore… they did.

We were finally granted the honor and privilege of finding out the specifics, a limited one-time Federal Reserve view, of a secret taxpayer funded “backdoor bailout” by a small group of unelected bankers. This data release reveals “emergency lending programs” that doled out $12.3 TRILLION in taxpayer money – $3.3 trillion in liquidity, $9 trillion in “other financial arrangements.”

Wait, what? Did you say $12.3 TRILLION tax dollars were thrown around in secrecy by unelected bankers… and Congress didn’t know any of the details?

Yes. The Founding Fathers are rolling over in their graves. The original copy of the Constitution spontaneously burst into flames. The ghost of Tom Paine went running, stark raving mad screaming through the halls of Congress.

The Federal Reserve was secretly throwing around our money in unprecedented fashion, and it wasn’t just to the usual suspects like Goldman Sachs, JP Morgan, Citigroup, Bank of America, etc.; it was to the entire Global Banking Cartel. To central banks throughout the world: Australia, Denmark, Japan, Mexico, Norway, South Korea, Sweden, Switzerland, England… To the Fed’s foreign primary dealers like Credit Suisse (Switzerland), Deutsche Bank (Germany), Royal Bank of Scotland (U.K.), Barclays (U.K.), BNP Paribas (France)… All their Ponzi players were “gifted.” All the Racketeer Influenced and Corrupt Organizations got their cut.

Talk about the ransacking and burning of Rome! Sayonara American middle class…

If you still had any question as to whether or not the United States is now the world’s preeminent banana republic, the final verdict was just delivered and the decision was unanimous. The ayes have it.

Any fairytale notions that we are living in a nation built on the rule of law and of the global economy being based on free market principles has now been exposed as just that, a fairytale. This moment is equivalent to everyone in Vatican City being told, by the Pope, that God is dead.

I’ve been arguing for years that the market is rigged and that the major Wall Street firms are elaborate Ponzi schemes, as have many other people who built their beliefs on rational thought, reasoned logic and evidence. We already came to this conclusion by doing the research and connecting the dots. But now, even our strongest skeptics and the most ardent Wall Street supporters have it all laid out in front of them, on FEDERAL RESERVE SPREADSHEETS.

Even the Financial Times, which named Lloyd Blankfein its 2009 person of the year, reacted by reporting this: “The initial reactions were shock at the breadth of lending, particularly to foreign firms. But the details paint a bleaker and even more disturbing picture.”

Yes, the emperor doesn’t have any clothes. God is, indeed, dead. But, for the moment at least, the illusion continues to hold power. How is this possible?

To start with, as always, the US television “news” media (propaganda) networks just glossed over the whole thing – nothing to see here, just move along, back after a message from our sponsors… Other than that obvious reason, I’ve come to the realization that the Federal Reserve’s crimes are so big, so huge in scale, it is very hard for people to even wrap their head around it and comprehend what has happened here.

Think about it. In just this one peek we got at its operations, we learned that the Fed doled out $12.3 trillion in near-zero interest loans, without Congressional input.

The audacity and absurdity of it all is mind boggling…

Based on many conversations I’ve had with people, it seems that the average person doesn’t comprehend how much a trillion dollars is, let alone 12.3 trillion. You might as well just say 12.3 gazillion, because people don’t grasp a number that large, nor do they understand what would be possible if that money was used in other ways.

Can you imagine what we could do to restructure society with $12.3 trillion? Think about that…

People also can’t grasp the colossal crime committed because they keep hearing the word “loans.” People think of the loans they get. You borrow money, you pay it back with interest, no big deal.

That’s not what happened here. The Fed doled out $12.3 trillion in near-zero interest loans, using the American people as collateral, demanding nothing in return, other than a bunch of toxic assets in some cases. They only gave this money to a select group of insiders, at a time when very few had any money because all these same insiders and speculators crashed the system.

Do you get that? The very people most responsible for crashing the system, were then rewarded with trillions of our dollars. This gave that select group of insiders unlimited power to seize control of assets and have unprecedented leverage over almost everything within their economies – crony capitalism on steroids.

This was a hostile world takeover orchestrated through economic attacks by a very small group of unelected global bankers. They paralyzed the system, then were given the power to recreate it according to their own desires. No free market, no democracy of any kind. All done in secrecy. In the process, they gave themselves all-time record-breaking bonuses and impoverished tens of millions of people – they have put into motion a system that will inevitably collapse again and utterly destroy the very existence of what is left of an economic middle class.

That is not hyperbole. That is what happened.

We are talking about trillions of dollars secretly pumped into global banks, handpicked by a small select group of bankers themselves. All for the benefit of those bankers, and at the expense of everyone else. People can’t even comprehend what that means and the severe consequences that it entails, which we have only just begun to experience.

Let me sum it up for you: The American Dream is O-V-E-R.

Welcome to the neo-feudal-fascist state.

People throughout the world who keep using the dollar are either A) Part of the scam; B) Oblivious to reality; C) Believe that US military power will be able to maintain the value of an otherwise worthless currency; D) All of the above.

No matter which way you look at it, we are all in serious trouble!

If you are an elected official, (I know at least 17 of you subscribe to my newsletter) and you believe in the oath you took upon taking office, you must immediately demand a full audit of the Federal Reserve and have Ben Bernanke and the entire Federal Reserve Board detained. If you are not going to do that, you deserve to have the words “Irrelevant Puppet” tattooed across your forehead.

Yes, those are obviously strong words, but they are the truth.

The Global Banking Cartel has now been so blatantly exposed, you cannot possibly get away with pretending that we live in a nation of law based on the Constitution. The jig is up.

It’s been over two years now; does anyone still seriously not understand why we are in this crisis? Our economy has been looted and burnt to the ground due to the strategic, deliberate decisions made by a small group of unelected global bankers at the Federal Reserve. Do people really not get the connection here? I mean, H.E.L.L.O. Our country is run by an unelected Global Banking Cartel.

I am constantly haunted by a quote from Harry Overstreet, who wrote the following in his 1925 groundbreaking study Influencing Human Behavior: “Giving people the facts as a strategy of influence” has been a failure, “an enterprise fraught with a surprising amount of disappointment.”

This crisis overwhelmingly proves Overstreet’s thesis to be true. Nonetheless, we solider on…

Here’s a roundup of reports on this BernankeLeaks:

Prepare to enter the theater of the absurd…

I’ll start with Senator Bernie Sanders (I-Vermont). He was the senator who Bernanke blew off when he was asked for information on this heist during a congressional hearing. Sanders fought to get the amendment written into the financial “reform” bill that gave us this one-time peek into the Fed’s secret operations. (Remember, remember the 6th of May, HFT, flash crash and terrorism. “Hey, David, Homeland Security is on the phone! They want to ask you questions about some NYSE SLP program.”)

In an article entitled, “A Real Jaw-Dropper at the Federal Reserve,” Senator Sanders reveals some of the details:At a Senate Budget Committee hearing in 2009, I asked Fed Chairman Ben Bernanke to tell the American people the names of the financial institutions that received an unprecedented backdoor bailout from the Federal Reserve, how much they received, and the exact terms of this assistance. He refused. A year and a half later… we have begun to lift the veil of secrecy at the Fed…In an article entitled, “The Fed Lied About Wall Street,” Zach Carter sums it up this way:

After years of stonewalling by the Fed, the American people are finally learning the incredible and jaw-dropping details of the Fed’s multi-trillion-dollar bailout of Wall Street and corporate America….

We have learned that the $700 billion Wall Street bailout… turned out to be pocket change compared to the trillions and trillions of dollars in near-zero interest loans and other financial arrangements the Federal Reserve doled out to every major financial institution in this country.…

Perhaps most surprising is the huge sum that went to bail out foreign private banks and corporations including two European megabanks — Deutsche Bank and Credit Suisse — which were the largest beneficiaries of the Fed’s purchase of mortgage-backed securities….

Has the Federal Reserve of the United States become the central bank of the world?… [read Global Banking Cartel]

What this disclosure tells us, among many other things, is that despite this huge taxpayer bailout, the Fed did not make the appropriate demands on these institutions necessary to rebuild our economy and protect the needs of ordinary Americans….

What we are seeing is the incredible power of a small number of people who have incredible conflicts of interest getting incredible help from the taxpayers of this country while ignoring the needs of the people. [read more]The Federal Reserve audit is full of frightening revelations about U.S. economic policy and those who implement it… By denying the solvency crisis, major bank executives who had run their companies into the ground were allowed to keep their jobs, and shareholders who had placed bad bets on their firms were allowed to collect government largesse, as bloated bonuses began paying out soon after.Even the Financial Times is jumping ship:

But the banks themselves still faced a capital shortage, and were only kept above those critical capital thresholds because federal regulators were willing to look the other way, letting banks account for obvious losses as if they were profitable assets.

So based on the Fed audit data, it’s hard to conclude that Fed Chairman Ben Bernanke was telling the truth when he told Congress on March 3, 2009, that there were no zombie banks in the United States.

“I don’t think that any major U.S. bank is currently a zombie institution,” Bernanke said.

As Bernanke spoke those words banks had been pledging junk bonds as collateral under Fed facilities for several months…

This is the heart of today’s foreclosure fraud crisis. Banks are foreclosing on untold numbers of families who have never missed a payment, because rushing to foreclosure generates lucrative fees for the banks, whatever the costs to families and investors. This is, in fact, far worse than what Paul Krugman predicted. Not only are zombie banks failing to support the economy, they are actively sabotaging it with fraud in order to make up for their capital shortages. Meanwhile, regulators are aggressively looking the other way.

The Fed had to fix liquidity in 2008. That was its job. But as major banks went insolvent, the Fed and Treasury had a responsibility to fix that solvency issue—even though that meant requiring shareholders and executives to live up to losses. Instead, as the Fed audit tells us, policymakers knowingly ignored the real problem, pushing losses onto the American middle class in the process.” [read more]Sunlight Shows Cracks in Fed’s Rescue StoryIn true Fed fashion, they didn’t even fully comply with Congress. In a report entitled, “Fed Withholds Collateral Data for $885 Billion in Financial-Crisis Loans,” Bloomberg puts some icing on the cake:

It took two years, a hard-fought lawsuit, and an act of Congress, but finally… the Federal Reserve disclosed the details of its financial crisis lending programs. The initial reactions were shock at the breadth of lending, particularly to foreign firms. But the details paint a bleaker, earlier, and even more disturbing picture…. An even more troubling conclusion from the data is that… it is now apparent that the Fed took on far more risk, on less favorable terms, than most people have realized. [read more]For three of the Fed’s six emergency facilities, the central bank released information on groups of collateral it accepted by asset type and rating, without specifying individual securities. Among them was the Primary Dealer Credit Facility, created in March 2008 to provide loans to brokers as Bear Stearns Cos. collapsed.See also:

“This is a half-step,” said former Atlanta Fed research director Robert Eisenbeis, chief monetary economist at Cumberland Advisors Inc. in Sarasota, Florida. “If you were going to audit the facilities, then would this enable you to do an audit? The answer is ‘No,’ you would have to go in and look at the individual amounts of collateral and how it was broken down to do that. And that is the spirit of what the requirements were in Dodd-Frank.” [read more]Fed Data Dump Reveals More Contradictions About its $1.25 Trillion MBS Purchase Program Fed Created Conflicts in Improvising $3.3 Trillion Financial System Rescue Meet The 35 Foreign Banks That Got Bailed Out By The Fed Ben Bernanke’s Secret Global Bank Here’s the only person on US TV “news” who actually covers and understands any of this, enter Dylan Ratigan, with his guest Chris Whalen from Institutional Risk Analytics. This quote from Whalen sums it up well: “The folks at the Fed have become so corrupt, so captured by the banking industry… the Fed is there to support the speculators and they let the real economy go to hell.”The Progressive’s Matthew Rothschild has a good quote: “The financial bailout was a giant boondoggle, undemocratic and kleptocratic to its core.”

Matt Stoller on NewDeal 2.0:End This FedIn case anyone is confused into believing that this is just another right vs. left partisan issue, enter Fox Business host Judge Andrew Napolitano with his guest Republican Congressman Ron Paul, who is, of course, a longtime leading Fed critic. Paul hopes to see some Wikileaks on the Federal Reserve:

The Fed, and specifically the people who run it, are responsible for declining wages, for de-industrialization, for bubbles, and for the systemic corruption of American capital markets. The new financial blogosphere destroyed the Fed’s mythic stature…. With a loss of legitimacy comes a lack of public trust and a vulnerability to any form of critic. The Fed is now less respected than the IRS…. Liberals should stop their love affair with conservative technocratic myths of monetary independence, and cease seeing this Federal Reserve as a legitimate actor. At the very least, we need to begin noticing that these people do in fact run the country, and should not. [read more]The Sunlight Foundation shines a light on Bank of America and the Federal Reserve’s brother money manager BlackRock: Federal Reserve Loan Program Allowed Bank of America to Benefit TwiceGretchen Morgenson at the New York Times jumps into the act:

Bank of America was one of several banks that was able to play both sides of a Federal Reserve program launched during the 2008 financial crisis. While Bank of America was selling its assets to firms obtaining loans through the Fed program, the investment firm BlackRock—partially owned by Bank of America—was potentially turning a profit by using those loans to buy assets similar to those sold by Bank of America. [read more]So That’s Where the Money WentWelcome to the “global pawnshop:”

How the truth shines through when you shed a little light on a subject….

All of the emergency lending data released by the Fed are highly revealing, but why weren’t they made public much earlier? That’s a question that Walker F. Todd, a research fellow at the American Institute for Economic Research, is asking.

Mr. Todd, a former assistant general counsel and research officer at the Federal Reserve Bank of Cleveland, said details about the Fed’s vast and various programs should have been available before the Dodd-Frank regulatory reform law was even written.

“The Fed’s current set of powers and the shape of the Dodd-Frank bill over all might have looked quite different if this information had been made public during the debate on the bill,” he said. “Had these tables been out there, I think Congress would have either said no to emergency lending authority or if you get it, it’s going to be a much lower number — half a trillion dollars in the aggregate.” [read more]The Fed Operates as a “global pawnshop:” $9 trillion to 18 financial institutions“No strings attached.” Financial reporter Barry Grey unleashes the truth:

What the report shows is that the Fed operated as a global pawnshop taking in practically anything the banks had for collateral. What is even more disturbing is that the Federal Reserve did not enact any punitive charges to these borrowers so you had banks like Goldman Sachs utilizing the crisis to siphon off cheap collateral. The Fed is quick to point out that “taxpayers were fully protected” but mention little of the destruction they have caused to the US dollar. This is a hidden cost to Americans and it also didn’t help that they were the fuel that set off the biggest global housing bubble ever witnessed by humanity. [read more]Fed report lifts lid on Great Bank Heist of 2008-2009Here’s an old Jim Rogers interview from two years ago when this whole thing was originally going down:

The banks and corporations that benefited were not even obliged to provide an account of what they did with the money. The entire purpose of the operation was to use public funds to cover the gambling losses of the American financial aristocracy, and create the conditions for the financiers and speculators to make even more money.

All of the 21,000 transactions cited in the Fed documents―released under a provision included, over the Fed’s objections, in this year’s financial regulatory overhaul bill―were carried out in secret. The unelected central bank operated without any congressional mandate or oversight.

The documents shed light on the greatest plundering of social resources in history. It was carried out under both the Republican Bush and Democratic Obama administrations. Those who organized the looting of the public treasury were long-time Wall Street insiders: men like Bush’s treasury secretary and former Goldman Sachs CEO Henry Paulson and the then-president of the New York Federal Reserve, Timothy Geithner….

The Fed documents show that the US central bank enabled banks and corporations to offload their bad debts onto the Fed’s balance sheet. Now, in order to prevent a collapse of the dollar and a default by the US government, the American people are being told they must sacrifice to reduce the national debt and budget deficit.

But as the vast sums make clear, the “sacrifice” being demanded of working people means their impoverishment―wage-cutting, mass unemployment, cuts in health care, Social Security, Medicare, Medicaid, etc.

The very scale of the Fed bailout points to the scale of the financial crash and the criminality that fostered it…. The entire US capitalist economy rested on a huge Ponzi scheme that was bound to collapse…

The banks were able to take the cheap cash from the Fed and lend it back to the government at double and quadruple the interest rates they were initially charged―pocketing many billions in the process….

The ongoing saga of the looting of the economy by the financial elite puts the lie to the endless claims that “there is no money” for jobs, housing, education or health care. The ruling class is awash in money. [read more]Here are two videos that I made last year, with an assist from Alan Grayson and Dylan Ratigan:

The Wall Street Economic Death Squad – Part IThe Greatest Theft in History – Wall Street Economic Death Squad – Part II And on a final note, you may as well rock out to this new song while Rome burns…